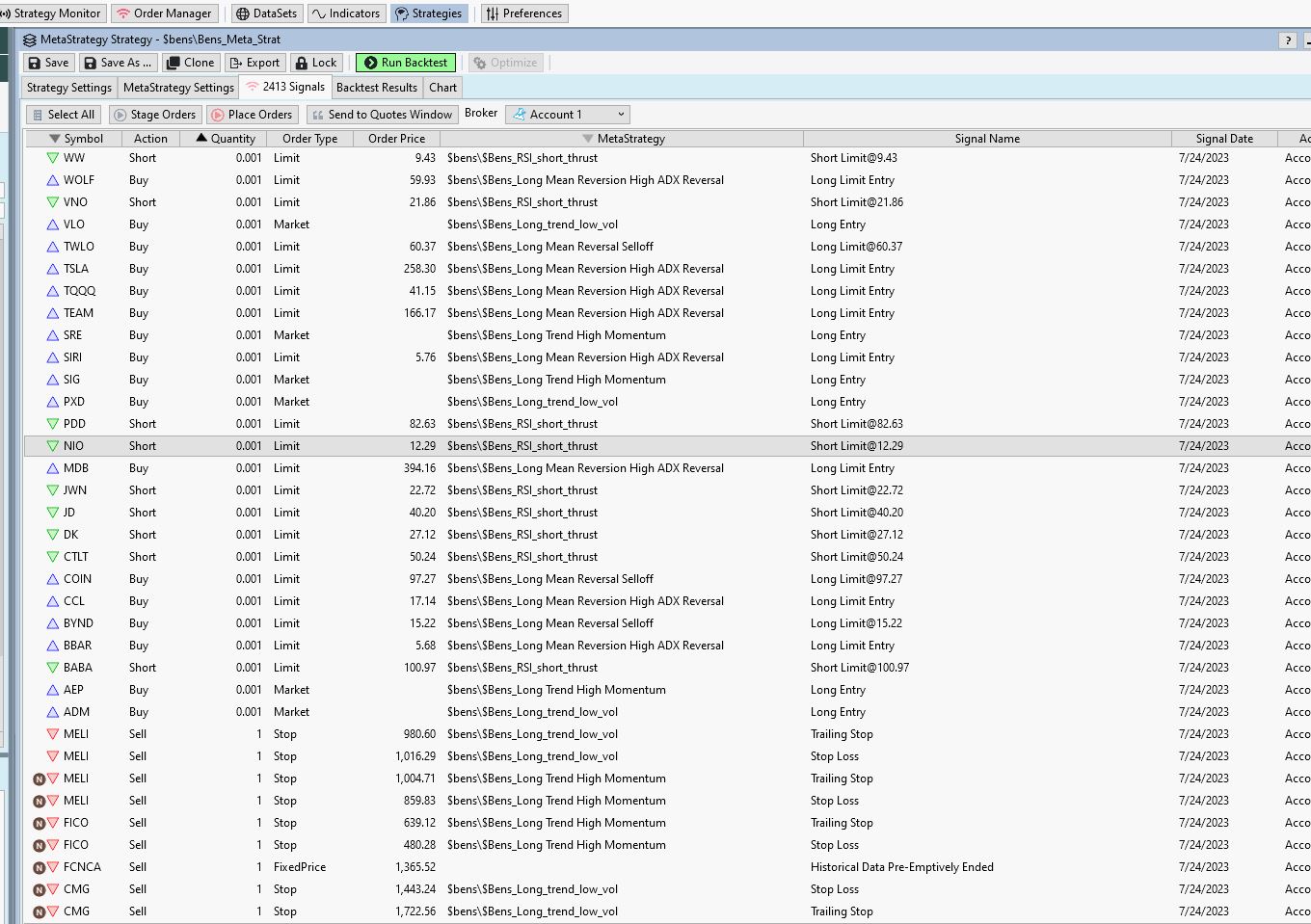

Greetings, I am working on backtests using the WL published Bensdorp strategies by DrKoch. Using the metastrategy framework with the entire Nasdaq and NYSE as a dataset(yahoo) and the original portfolio weights, metastrategy output signals produce order quantities of .001 shares. Furthermore after clicking on the signal to observe the signals on a chart there appears to be open orders of different quantities (unsure if this is related). I am new to wealthlab so forgive me if there is an obvious fix. Also, any recommendations or directions to documentation on the best way to implement the tracking of signals from metastrategies that use large data sets would be greatly appreciated.

Special thanks to DrKoch and WL for making the Bensdorp strategies available saved me untold hours of work and it is much appreciated.

#signals generated on 7/24/2023

# for clarity all the setting should be the same as the original DrKoch post except for the data set.

price

# NIO chart showing .001 limit (short) order and sell stop for 204 shares at a lower

Special thanks to DrKoch and WL for making the Bensdorp strategies available saved me untold hours of work and it is much appreciated.

#signals generated on 7/24/2023

# for clarity all the setting should be the same as the original DrKoch post except for the data set.

price

# NIO chart showing .001 limit (short) order and sell stop for 204 shares at a lower

Rename

Clearly it's an issue with one of the following:

1. the Max Risk % Limited to % of Equity Position Sizer

2. the sizers' configuration/parameters

3. the placement of the MaxRisk stop level

The strategies use GetMaxRiskStopLevel(), so probably not #3.

We'll assume #1 is correct for now, which leaves the configuration of the sizer.

What is it?

1. the Max Risk % Limited to % of Equity Position Sizer

2. the sizers' configuration/parameters

3. the placement of the MaxRisk stop level

The strategies use GetMaxRiskStopLevel(), so probably not #3.

We'll assume #1 is correct for now, which leaves the configuration of the sizer.

What is it?

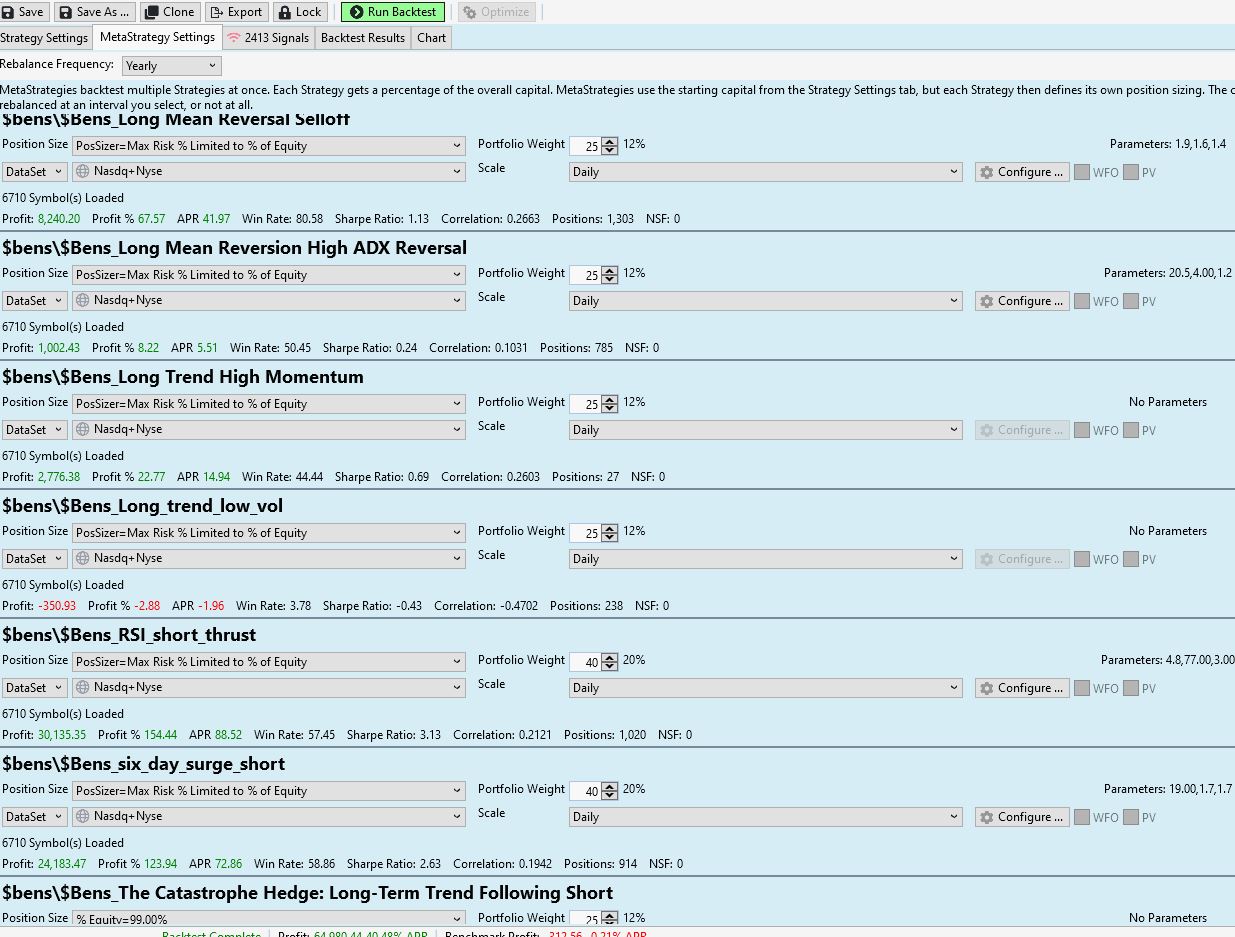

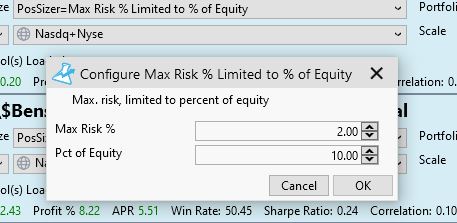

Thanks for your response, the position sizer is set a 2% max risk with max of 10% of equity. Margin factor is set to 1 for the metastrategy.

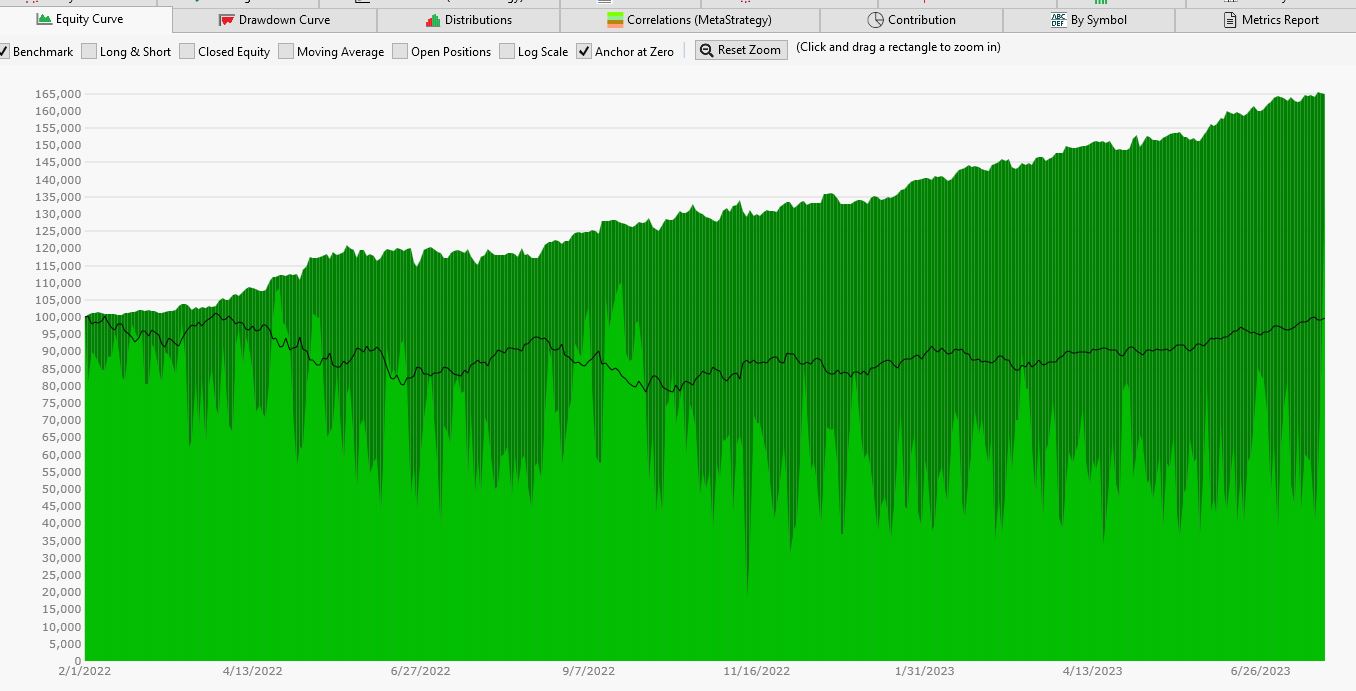

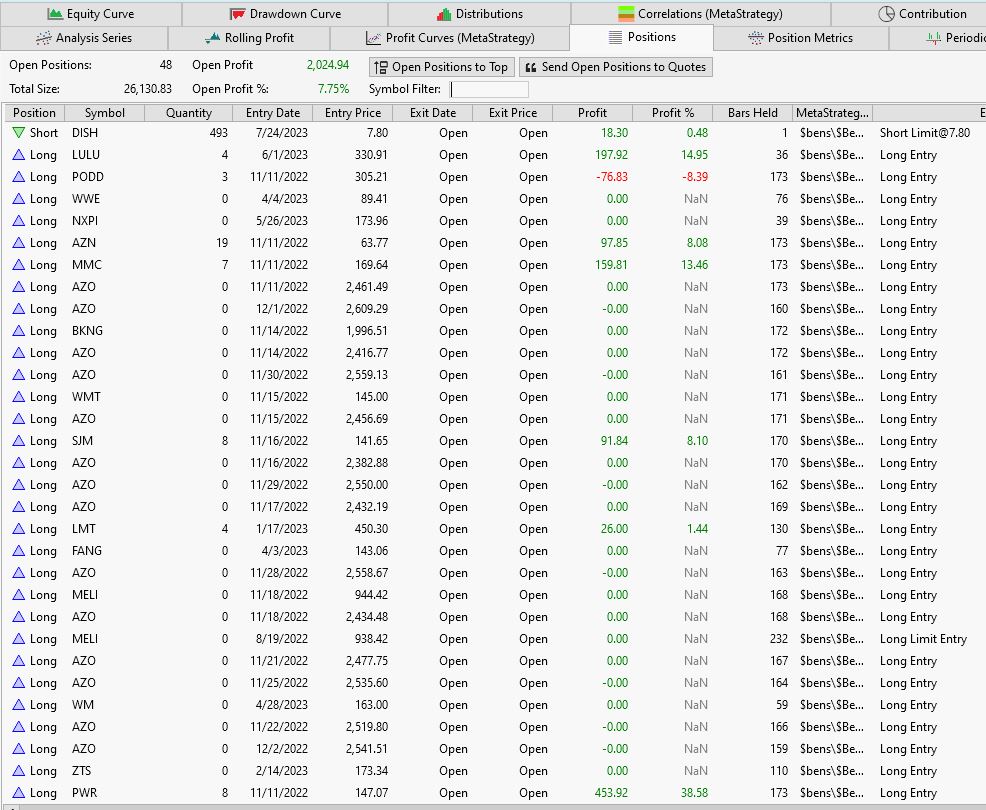

This is equity curve from the current backtest, which seems to have plenty of available cash.

Under the positions tab the issue also seems to have occurred where quantities of 0 are observed. This however does not seem to effect the final backtest results as far as I can tell.

Thanks

This is equity curve from the current backtest, which seems to have plenty of available cash.

Under the positions tab the issue also seems to have occurred where quantities of 0 are observed. This however does not seem to effect the final backtest results as far as I can tell.

Thanks

What extension is that sizer from?

Probably based on the Limited to 10% of equity sizing, my guess is that your risk level is too high. Try something more like 1% or even 0.5% Max Risk and see if it changes.

Either way, whoever knows something about that sizer needs to speak up!

Probably based on the Limited to 10% of equity sizing, my guess is that your risk level is too high. Try something more like 1% or even 0.5% Max Risk and see if it changes.

Either way, whoever knows something about that sizer needs to speak up!

The position sizer I believe is a part of the finantic.Indicators extension. I did re run the back test using the standard percent of equity at 10% and the .001 issue seems to have disappeared. However would note that using 2% risk with 10% equity is highly preferable. Going to test your suggestion of changing the % equity on the custom sizer now. Thanks!

Just tried a number of variations on the position sizer in question (1%r / 10%, 0.5%r/ 5%, 1%r / 5%) all return the .001 quantity in signals. Is it possible to hard code risk parameters in terms of sizing rather than using the position size settings? Also the signals tab generates NSF positions in metastategies whether "retain NSF positions" is checked or not. My main goal here is generate the correct positions and sizing on a daily basis. Thanks in advance.

QUOTE:I don't know anything about that Sizer, but this sounds like a bug to me.

all return the .001 quantity in signals.

QUOTE:I don't know which risk parameters you mean, but there are at least 20 sizers to choose from. Try the standard Max Risk Percent Sizer, use 0.5%, then I can help you.

Is it possible to hard code risk parameters in terms of sizing rather than using the position size settings?

QUOTE:It's in the User Guide: MetaStrategies run with Retain NSF Positions enabled and is not optional.

Also the signals tab generates NSF positions in metastategies whether "retain NSF positions" is checked or not.

I appreciate your help.

FWIW, this sounds very similar to a problem I was having earlier this spring. See https://www.wealth-lab.com/Discussion/Finantic-Max-Risk-Limited-to-of-Equity-returns-incorrect-size-9794

That does appear to be the same issue. Did you ever come up with working solution?

It looks like you need Dr Koch to work on that Pos Sizer.

Please just switch to the Max Risk Percent sizer, use 0.5%, and let us know the result.

Please just switch to the Max Risk Percent sizer, use 0.5%, and let us know the result.

There is a rumor of at least a partial fix in WL8-B40. But I also think that Finantic has a fix to their position sizer needed.

Yes indeed if Dr Koch could fix the position sizer that would be great. Ran 20 year back test using 2% max risk (stuck with 2% because if my math is correct this creates position sizes of .24% (L) and .4%(S) on a entire account basis when using the meta strategy.) the results still look very good. Also using the max risk % setting all position sizing issues seem to be fixed in metastrategy and strategy monitor.

However the lack of 10% equity position cap seems to be the primary cause of much of the short volatility post 2020.

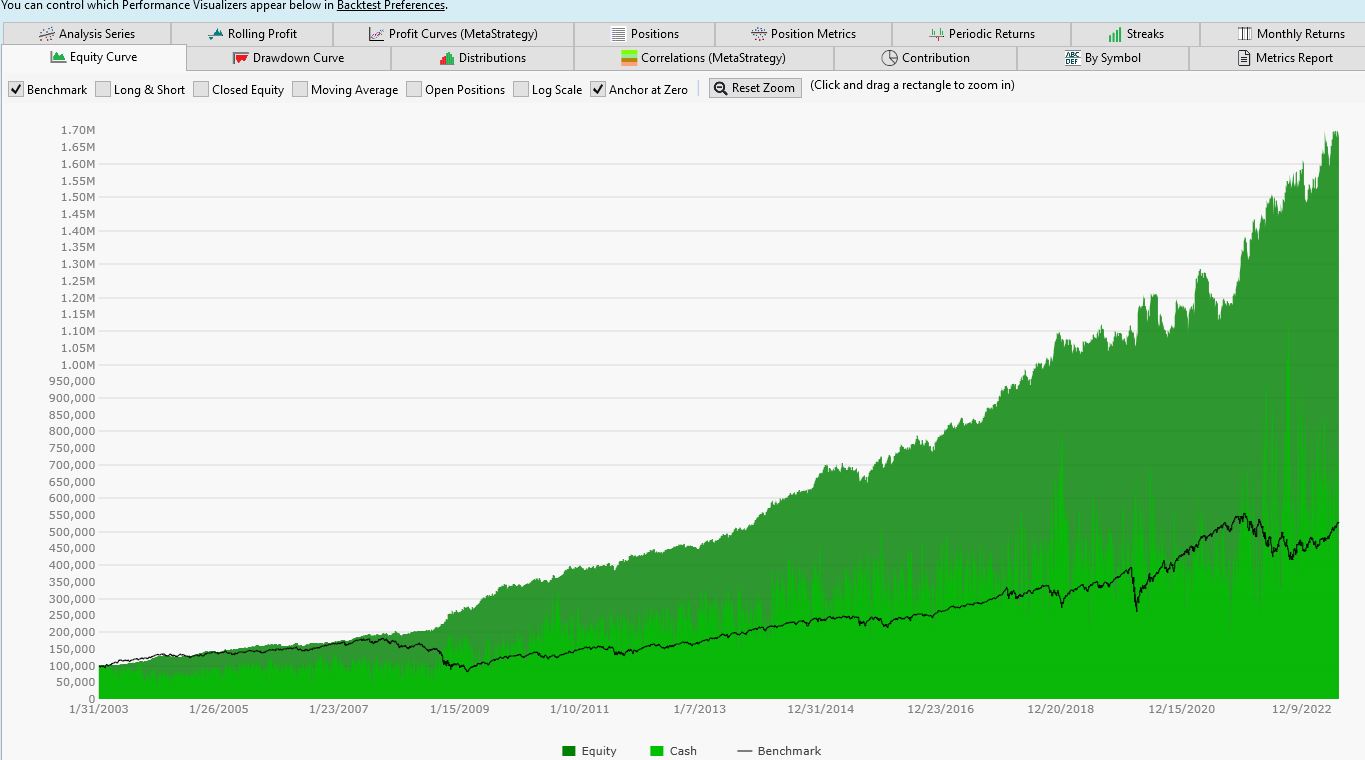

Here is a final equity curve of the stated back test.

Interestingly using the Dr Koch's position sizer during 20 year back tests, with the entire nasdaq and nyse data set, it comes very close to what Mr. Bensdorp discussed in his book and would be willing to assume that because the erroneously sized positions are so small that they had little effect on the back test results (sorry dont have screen shots of these but can re run in if anyone is interested). In conclusion it would be well worth it to have the max risk % / max equity % working. Thanks for the help.

However the lack of 10% equity position cap seems to be the primary cause of much of the short volatility post 2020.

Here is a final equity curve of the stated back test.

Interestingly using the Dr Koch's position sizer during 20 year back tests, with the entire nasdaq and nyse data set, it comes very close to what Mr. Bensdorp discussed in his book and would be willing to assume that because the erroneously sized positions are so small that they had little effect on the back test results (sorry dont have screen shots of these but can re run in if anyone is interested). In conclusion it would be well worth it to have the max risk % / max equity % working. Thanks for the help.

Your Response

Post

Edit Post

Login is required