Given my split settings, the difference between the start date of the first period and the end date of the last period should be 30 months. However, it is approximately 22 months. And in general, the partitioning settings are not respected.

I also noticed that in the "Tabular (WFO)" tab, the start date of the first period (and not only the first) does not match the date indicated in the split (02/24/2021 and 03/03/2021).

Among the minor bugs, I noticed that the split settings are not saved and are reset every time the "WFO Data Range Wizard" button is pressed.

I would like to be able to set the In-Sample Range and Out-of-Sample Range dates and the number of periods manually arbitrarily.

I am attaching the video:

https://drive.google.com/file/d/1_C3b20w3aeaMEjoDa9t4n3GDfguSdcHI/view?usp=sharing

I also noticed that in the "Tabular (WFO)" tab, the start date of the first period (and not only the first) does not match the date indicated in the split (02/24/2021 and 03/03/2021).

Among the minor bugs, I noticed that the split settings are not saved and are reset every time the "WFO Data Range Wizard" button is pressed.

I would like to be able to set the In-Sample Range and Out-of-Sample Range dates and the number of periods manually arbitrarily.

I am attaching the video:

https://drive.google.com/file/d/1_C3b20w3aeaMEjoDa9t4n3GDfguSdcHI/view?usp=sharing

Rename

When you configure the date range for "Most Recent N Months" WealthLab uses "today" as the basis for that. However, your data ends in 2022, so you're missing 7 or 8 months of data in that ASCII file.

Configure a specific date range with the dates that your data covers.

Configure a specific date range with the dates that your data covers.

QUOTE:I agree, that's annoying! I'll mark that to investigate/fix.

.. the split settings are not saved and are reset every time the "WFO Data Range Wizard" button is pressed.

Cone, hello!

I set the exact time frame for the test. This didn't help solve the problem. Moreover, after the WFO test, the period settings are reset to "Most Recent N Months". In addition, there is still no explanation for the difference in the dates of the beginning of the first period.

Attached video:

https://drive.google.com/file/d/1Q_iZ7_jdlYdrx-jUtKf4wwX6inPjzQ1q/view?usp=sharing

I set the exact time frame for the test. This didn't help solve the problem. Moreover, after the WFO test, the period settings are reset to "Most Recent N Months". In addition, there is still no explanation for the difference in the dates of the beginning of the first period.

Attached video:

https://drive.google.com/file/d/1Q_iZ7_jdlYdrx-jUtKf4wwX6inPjzQ1q/view?usp=sharing

I agree with you. It's starting the first OOS test about 8 months/periods too late, and it's not producing a division that you can clearly map out like this -

.. and as I step back and look at this picture, I noticed that I drew 4 IS periods and essentially only 3 OOS periods (green). The last set doesn't really count.

I think what the Wizard divides the data in such a way to attempt to give you the approximate ratio of OOS-to-IS that you set up. I'll map out what it's actually doing now...

.. and as I step back and look at this picture, I noticed that I drew 4 IS periods and essentially only 3 OOS periods (green). The last set doesn't really count.

I think what the Wizard divides the data in such a way to attempt to give you the approximate ratio of OOS-to-IS that you set up. I'll map out what it's actually doing now...

It looks like the Date Range suggestion was misplaced. The WFO wizard automatically adapts to use the frequency from "Specify Ranges in what Frequency". Say it's Months, as in your video. Then, it automatically switches that Data Range control to the "Most Recent" N - Months.

Yours is a pretty odd case, because you're doing WFO with data that ended 8 months ago.

I think the part that you and I missed is that WealthLab is automatically specifies your Data Range to accommodate the WFO settings - and it does it using a Most Recent period, which ends "today".

We'll update the guide to explain this better.

Yours is a pretty odd case, because you're doing WFO with data that ended 8 months ago.

I think the part that you and I missed is that WealthLab is automatically specifies your Data Range to accommodate the WFO settings - and it does it using a Most Recent period, which ends "today".

We'll update the guide to explain this better.

Cone, hello!

I managed to set the desired period following your explanations.

But why do the start dates of the first period differ in the Optimization Settings->Walk-Forward and Tabular (WFO) tabs?

I managed to set the desired period following your explanations.

But why do the start dates of the first period differ in the Optimization Settings->Walk-Forward and Tabular (WFO) tabs?

It's an approximation based on your [previously-selected] Data Range to fit number of intervals and OOS % to the "Most Recent n-[Frequency]". So you'll always get the number of intervals requested, but the actual amount of IS and OOS data will be changed to accommodate the intervals and the IS/OOS ratio.

I didn't quite understand your explanation of why the dates of the beginning of the period differ on different tabs.

I want to be able to set periods up to the day and set the start and end dates manually and not be tied to the IS/OOS ratio. This is critical to my strategy.

I want to be able to set periods up to the day and set the start and end dates manually and not be tied to the IS/OOS ratio. This is critical to my strategy.

You can't set up the periods manually.

How is it so critical to the strategy that you need to set it up "to the day"?

How is it so critical to the strategy that you need to set it up "to the day"?

The fact is that I work with gluing futures at the time of gluing a large gap occurs.

I want to avoid testing the strategy at this point.

I want to avoid testing the strategy at this point.

What does the Optimizer have to do with this? Over time, the industry has developed a number of methods to create continuous futures contracts. Put one of them into your service:

https://quantpedia.com/continuous-futures-contracts-methodology-for-backtesting/

https://quantpedia.com/continuous-futures-contracts-methodology-for-backtesting/

I think it's valid point. In contradiction with the article, I wouldn't backtest any continuous contract method that altered the history to smooth out rollovers - however, I would use a back-adjusted contract for indicators.

They start by asseting "If the contracts are just spliced together, the backtesting of the strategy with the spliced dataset is wrong." Well, that's correct if you don't consider the rollovers, but wrong if you do - which is what Denis is trying to do.

WFO for futures with a spliced contract isn't going to work properly without the ability to define the transitions..

They start by asseting "If the contracts are just spliced together, the backtesting of the strategy with the spliced dataset is wrong." Well, that's correct if you don't consider the rollovers, but wrong if you do - which is what Denis is trying to do.

WFO for futures with a spliced contract isn't going to work properly without the ability to define the transitions..

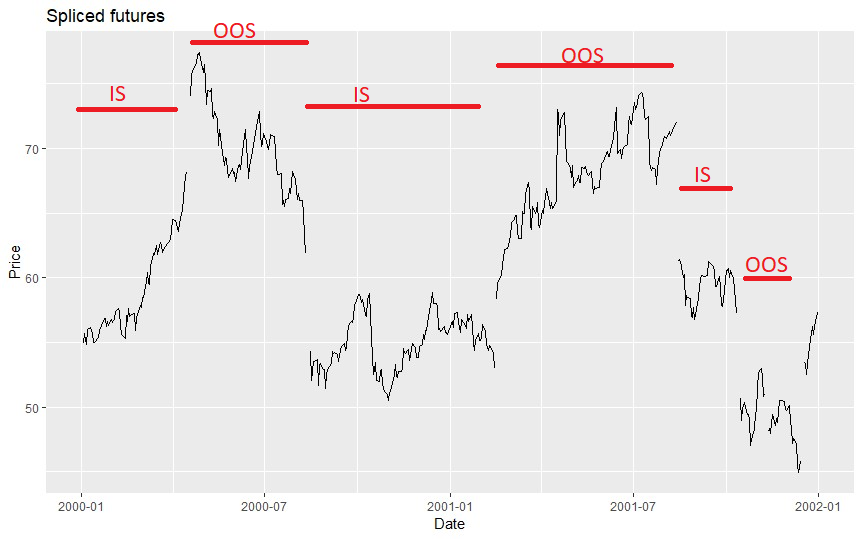

I did not understand most of what was written in the article at the link (regarding the methods for solving the problem) and by you. This is due to translation difficulties. In order to understand this, I need much more time. However, I am sending you a picture to illustrate how WFO period date management could solve this problem.

Even if WealthLab were aware of those dates, that model of IS /OOS is not going to happen. Why? Because older OOS periods later become part of the IS periods for both the Sliding and Expanding windows.

Listen Denis. We're not going to arrive where you want to go for this.

For your 1 symbol test, break up the dates and run your optimizations one by one, manually. You'll finish the analysis in no time at all, today.

Listen Denis. We're not going to arrive where you want to go for this.

For your 1 symbol test, break up the dates and run your optimizations one by one, manually. You'll finish the analysis in no time at all, today.

Your Response

Post

Edit Post

Login is required