Hi,

I'm confirming Signal and Open Postion is the same

Output two TXT files, [PreExecute] and [Execute]

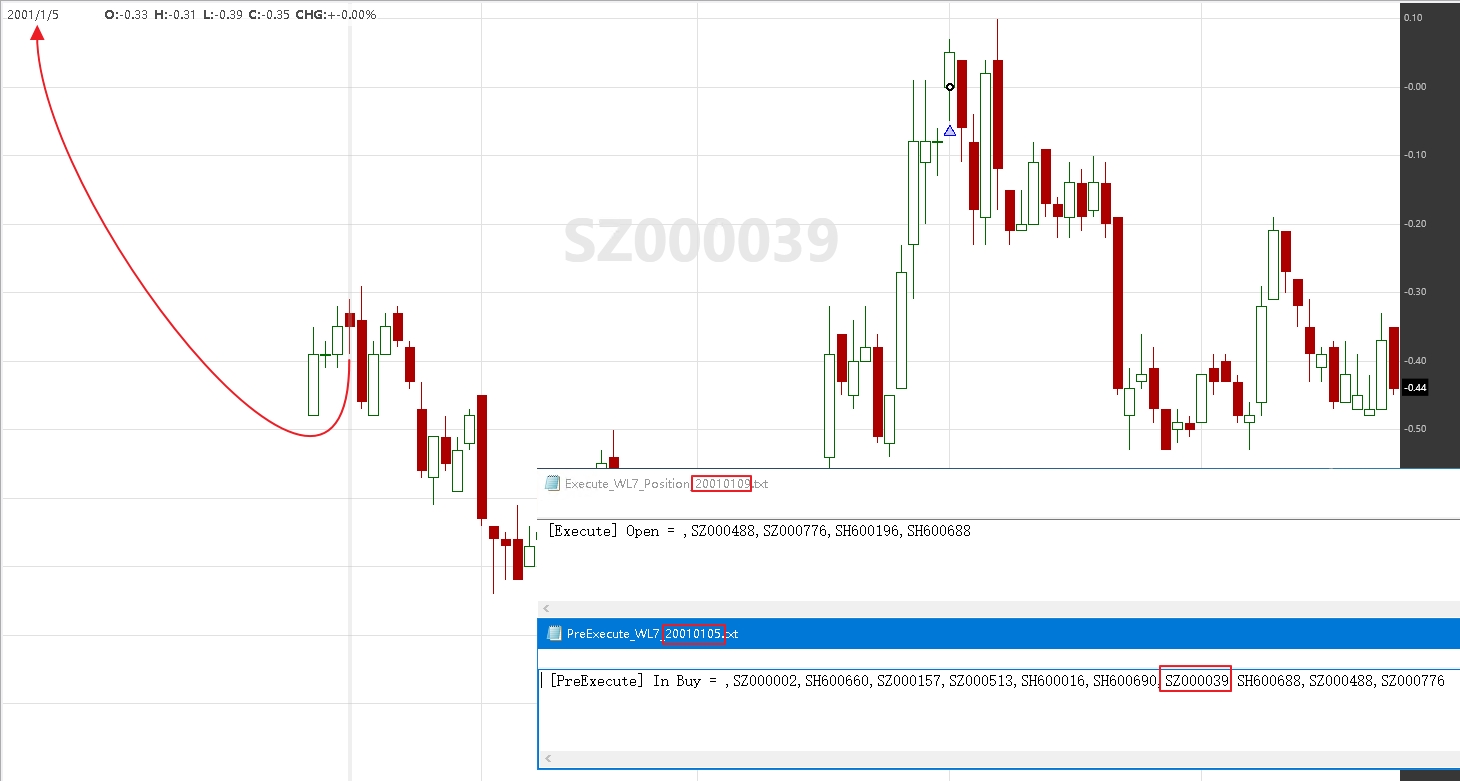

PreExecute_WL7_20010105.txt show Date 20010105 have ten symbols in buy list.

but into Backteset Results - Position tap sort by Entry Date

first Open Position on 2001/1/9, Why ?

I watch the SZ000039 symbol no signal on 2001/1/5 next bar

and missing a lot of signals from compare the two TXT files.

Chart:

Barcktest Results Position:

Code:

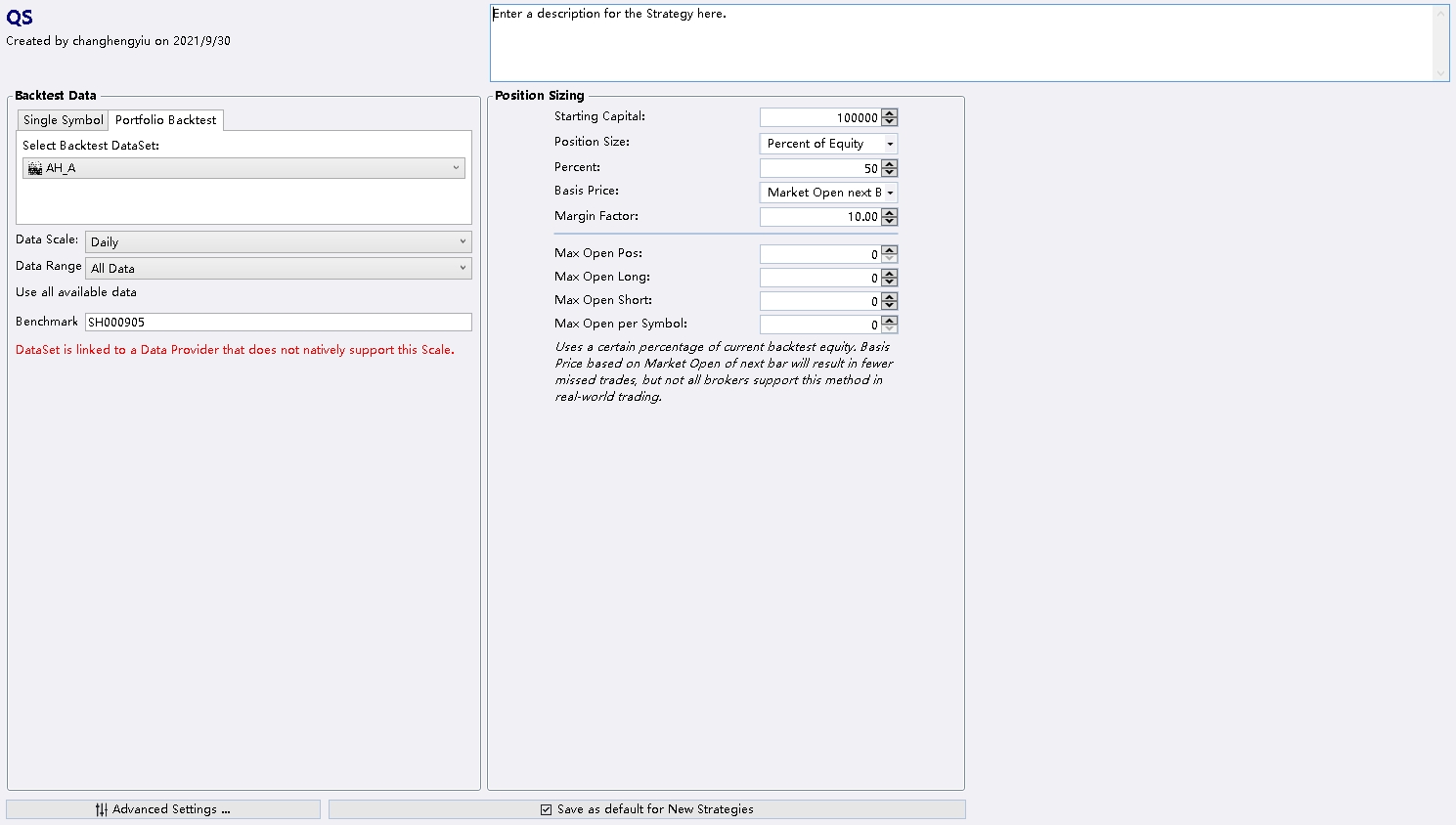

Strategy Setting:

I'm confirming Signal and Open Postion is the same

Output two TXT files, [PreExecute] and [Execute]

PreExecute_WL7_20010105.txt show Date 20010105 have ten symbols in buy list.

but into Backteset Results - Position tap sort by Entry Date

first Open Position on 2001/1/9, Why ?

I watch the SZ000039 symbol no signal on 2001/1/5 next bar

and missing a lot of signals from compare the two TXT files.

Chart:

Barcktest Results Position:

Code:

CODE:

using WealthLab.Backtest; using System; using WealthLab.Core; using WealthLab.Indicators; using System.Drawing; using System.Collections.Generic; using System.Linq; using System.IO; using System.Text; namespace WealthScript1 { public class Qs : UserStrategyBase { static List<BarHistory> Buys = new List<BarHistory>(); double StdVal; int idx; TimeSeries _Std; SMA _rSMA; private TimeSeries opL; //create indicators and other objects here, this is executed prior to the main trading loop public override void Initialize(BarHistory bars) { StartIndex = 100; _rSMA = new SMA(bars.Close, StartIndex); bars.Cache["_rSMA"] = _rSMA; opL = new TimeSeries(bars.DateTimes); } public override void PreExecute(DateTime dt, List<BarHistory> participants) { foreach (BarHistory bh in participants) { _Std = (SMA)bh.Cache["_rSMA"]; idx = GetCurrentIndex(bh); StdVal = _Std[idx]; bh.UserData = Math.Round(StdVal, 3); } participants.Sort((a, b) => a.UserDataAsDouble.CompareTo(b.UserDataAsDouble)); //Lowest --> Highest Buys.Clear(); for (int n = 0; n <= participants.Count - 1; n++) { if (Buys.Count == 10) break; if ((participants[n].UserDataAsDouble).ToString() != "NaN") Buys.Add(participants[n]); } FileStream fs = new FileStream(@"C:\Users\Administrator\Desktop\WL7_out\QS\WL7_" + dt.ToString("yyyyMMdd") + ".txt", FileMode.Create); StreamWriter sw = new StreamWriter(fs); sw.Write(" In Buy = "); foreach (BarHistory _strB in Buys) { sw.Write("," + _strB.Symbol); } sw.Flush(); sw.Close(); fs.Close(); } //execute the strategy rules here, this is executed once for each bar in the backtest history public override void Execute(BarHistory bars, int idx) { bool inBuyList = Buys.Contains(bars); var BuyListPctEquity = CurrentEquity * 0.05 / bars.Close[idx - 1]; opL[idx] = OpenPositionsAllSymbols.Where(t => t.EntryTransactionType.ToString() == "Buy").Count(); opL[idx] += Backtester.Orders.Where(l => l.PositionType == PositionType.Long && l.IsEntry).Count(); FileStream fs = new FileStream(@"C:\Users\Administrator\Desktop\WL7_out\QS\P\WL7_Position_" + bars.GetDate(idx).ToString("yyyyMMdd") + ".txt", FileMode.Create); StreamWriter sw = new StreamWriter(fs); List<Position> positions = GetPositionsAllSymbols(true); sw.Write(" Open = "); foreach (Position pos in positions) { if (pos.PositionType.ToString() == "Long") sw.Write("," + pos.Symbol); } sw.Flush(); sw.Close(); fs.Close(); if (inBuyList && opL[idx] <= 19) { if (!HasOpenPosition(bars, PositionType.Long)) { PlaceTrade(bars, TransactionType.Buy, OrderType.Market).Quantity = BuyListPctEquity; } } else if(!inBuyList) { if (HasOpenPosition(bars, PositionType.Long)) ClosePosition(LastPosition, OrderType.Market); } } } }

Strategy Setting:

Rename

Instruments that have negative prices don't exist. You can't trade them in real life or in a simulation either.

===== Edit: =====

Granted, we may have to rethink reality after last year when for a short time they were paying you to take crude oil deliveries... and then there are the negative yields in Europe...

===== Edit: =====

Granted, we may have to rethink reality after last year when for a short time they were paying you to take crude oil deliveries... and then there are the negative yields in Europe...

@Cone

Hi,

I'll revise the dataset.

problems remain unsolved.

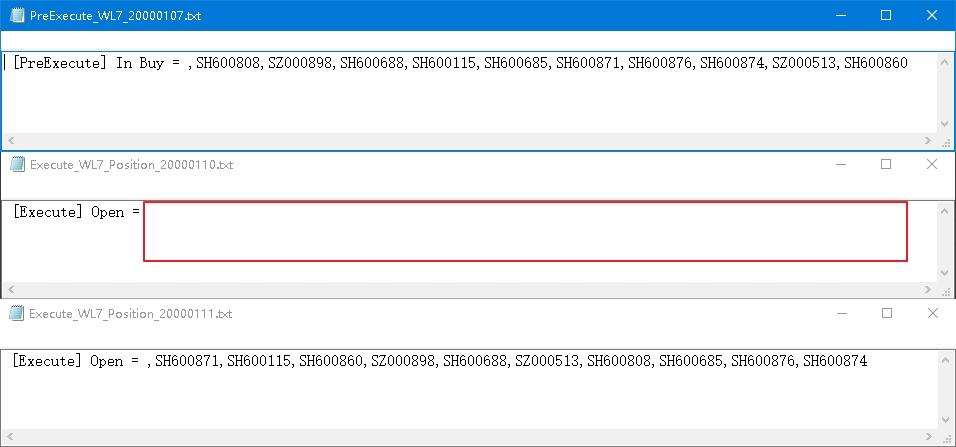

PreExecute_WL7_20000107.txt file

has ten symbols (SH600808,SZ000898,SH600688,SH600115,SH600685,SH600871,SH600876,SH600874,SZ000513,SH600860) in buy list.

no signal are displayed on the next trading day 2000 / 1 / 10

signal are displayed on 2000/1/11

Execute_WL7_Position_20000110.txt file is empty.

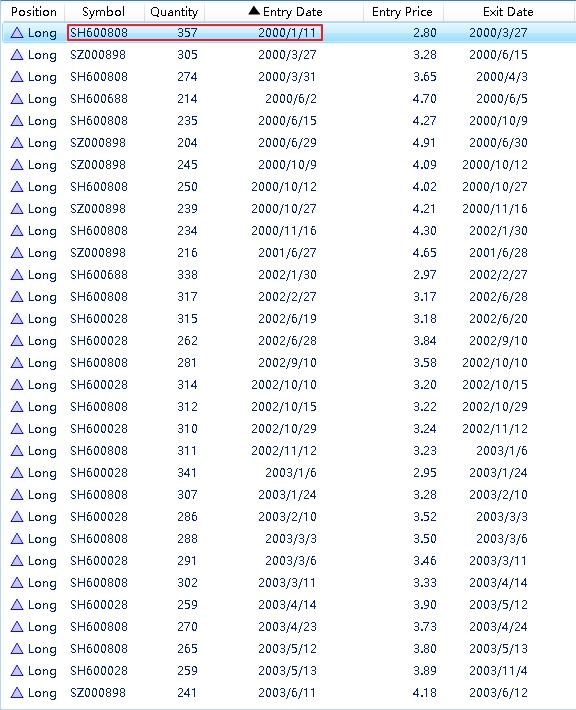

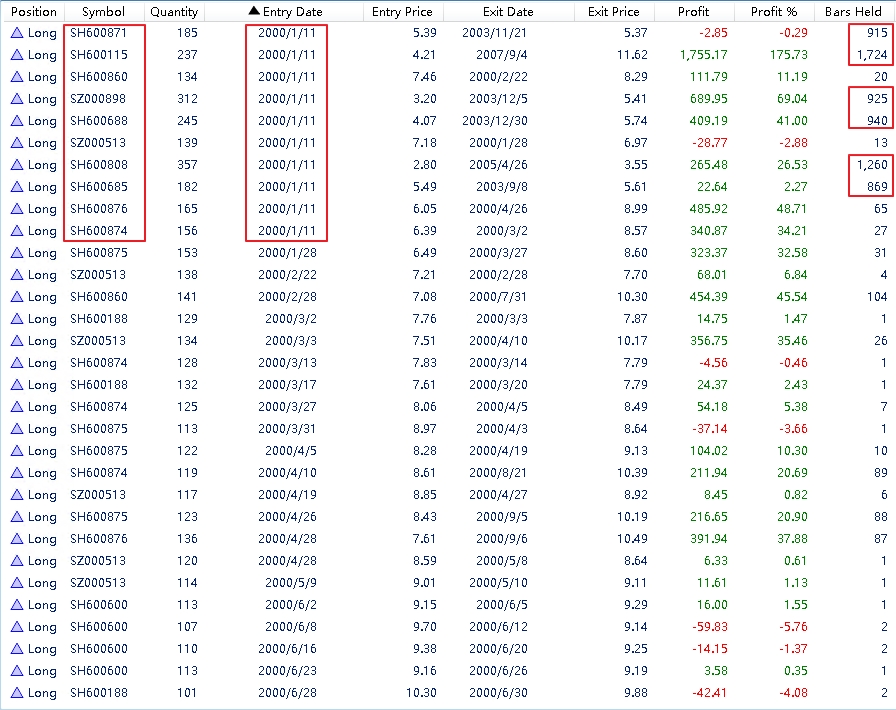

Backtest Results - Positions ( Sort by Entry Date)

and bars held unnormal.

strategy logic is checked several times.

Where is problem ?

Thx

Hi,

I'll revise the dataset.

problems remain unsolved.

PreExecute_WL7_20000107.txt file

has ten symbols (SH600808,SZ000898,SH600688,SH600115,SH600685,SH600871,SH600876,SH600874,SZ000513,SH600860) in buy list.

no signal are displayed on the next trading day 2000 / 1 / 10

signal are displayed on 2000/1/11

Execute_WL7_Position_20000110.txt file is empty.

Backtest Results - Positions ( Sort by Entry Date)

and bars held unnormal.

strategy logic is checked several times.

Where is problem ?

Thx

[Update]

Backtest Results - Positions ( Sort by Entry Date)

Backtest Results - Positions ( Sort by Entry Date)

One thing I noticed was the message in the Strategy Settings that the "DataSet is linked to a Data Provider that does not natively support this Scale."

The Scale is Daily. What Data Provider are you using that doesn't support the Daily scale?

The Scale is Daily. What Data Provider are you using that doesn't support the Daily scale?

Apparently, topic starter is using ASCII.

@Cone @Eugene

Hi,

Is using ASCII.

The first time I checked, there were symbols bars count = 0

then delete these symbols

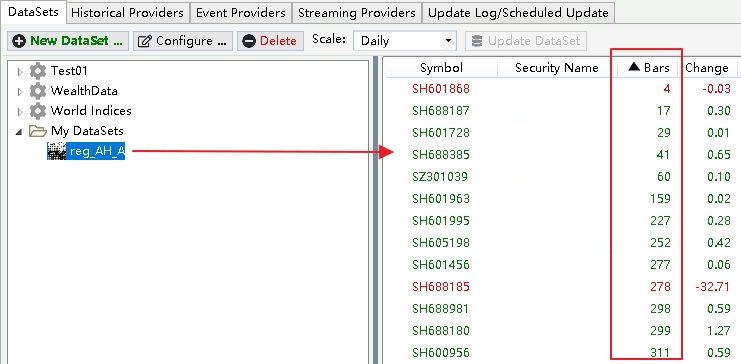

I double check dataset in Data Manager.

Sort ascending by bars count.

still shows doesn't support the Daily scale in Strategy Settings.

How to check the problem ?

Thx.

Hi,

Is using ASCII.

The first time I checked, there were symbols bars count = 0

then delete these symbols

I double check dataset in Data Manager.

Sort ascending by bars count.

still shows doesn't support the Daily scale in Strategy Settings.

QUOTE:

The Scale is Daily. What Data Provider are you using that doesn't support the Daily scale?

How to check the problem ?

Thx.

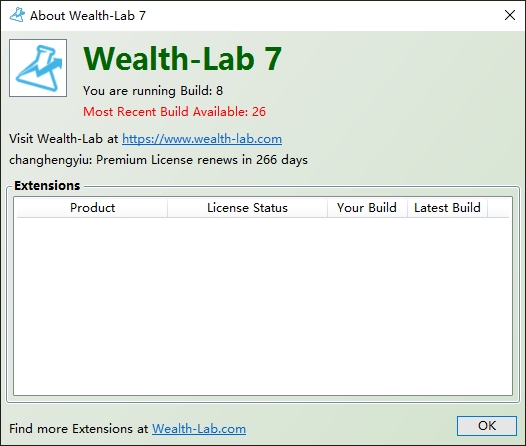

This issue is supposed to be fixed in build 26. I checked and you're running outdated builds 8 (!!!) and 21. Because they are not supported please upgrade both computers to the latest version.

@Eugene

Hi,

Where can i upgrade to latest version?

reinstall ?

Thx.

Hi,

Where can i upgrade to latest version?

reinstall ?

Thx.

Yes, simply download the new installer from Software > Download.

After upgrading the other PC please also check the Home Page tool inside WL7 for any outdated extensions it may have and download their upgraded installers from this page:

https://www.wealth-lab.com/Extension

After upgrading the other PC please also check the Home Page tool inside WL7 for any outdated extensions it may have and download their upgraded installers from this page:

https://www.wealth-lab.com/Extension

QUOTE:

ConeA

Sep 30, 2021, 03:24 AM - 12 days ago

#1

Instruments that have negative prices don't exist. You can't trade them in real life or in a simulation either.

===== Edit: =====

Granted, we may have to rethink reality after last year when for a short time they were paying you to take crude oil deliveries... and then there are the negative yields in Europe...

1 Best Answer

What about spreads (I'm guessing you can set up custom tickers for spreads, e.g. TM - 3*HMC)?

Wealth-Lab does not support negative prices. It will take a popular feature request to change that.

QUOTE:

Wealth-Lab does not support negative prices.

Then you won't be able to test strategies on some backadjusted futures.

In futures markets that spend a large time in backwardation, the back-adjustment process can cause historical prices to be pushed into negative territory.

That's right.

There are about a half-dozen methods you can use to back-adjust futures, and I wouldn't use any of them for backtesting. Use the continuous contract for the non-adjusted, real prices and a meta data file to trigger rollovers. Close and re-open positions on the rollover, just like you'd have to do for real trading.

There are about a half-dozen methods you can use to back-adjust futures, and I wouldn't use any of them for backtesting. Use the continuous contract for the non-adjusted, real prices and a meta data file to trigger rollovers. Close and re-open positions on the rollover, just like you'd have to do for real trading.

Your Response

Post

Edit Post

Login is required