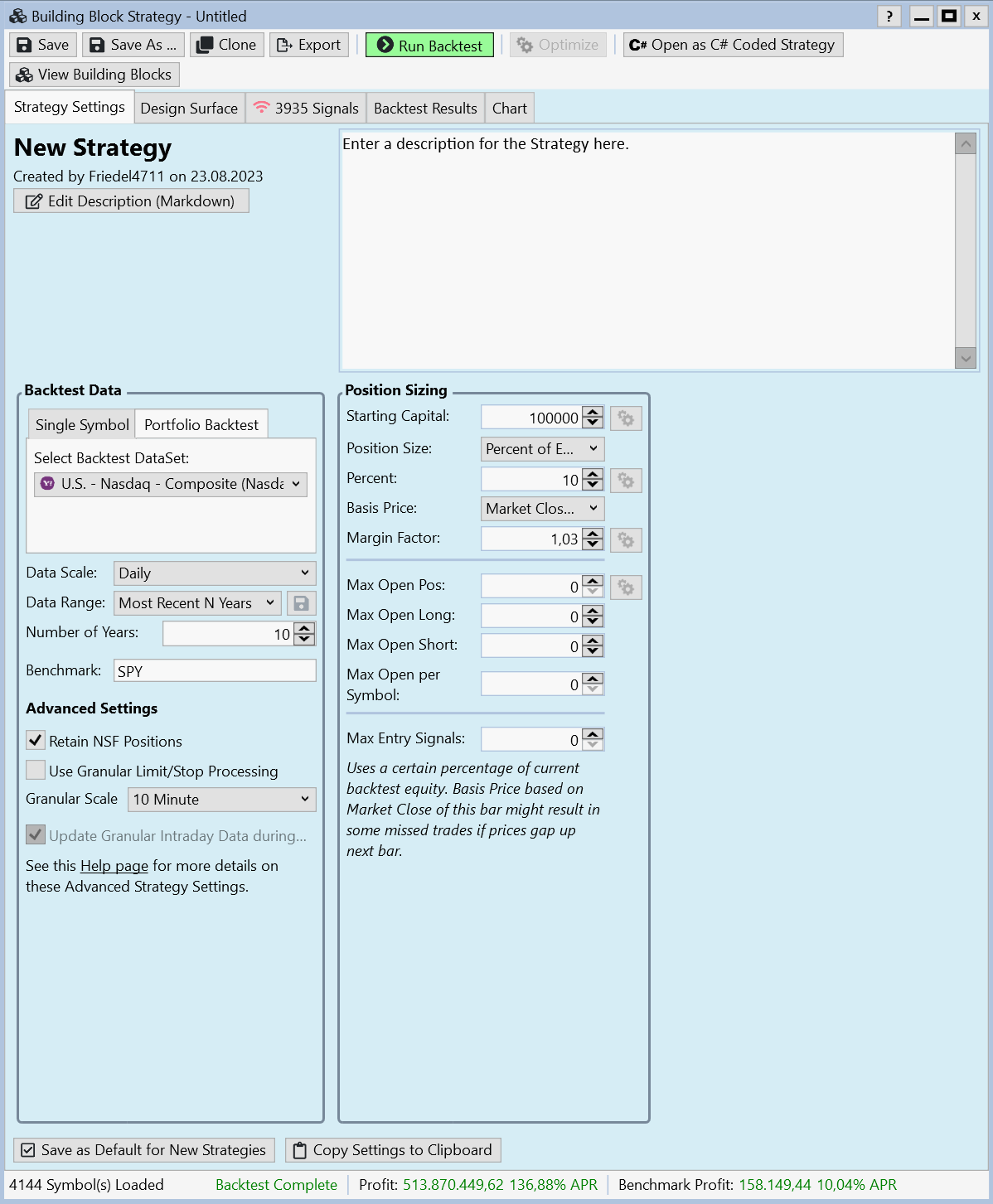

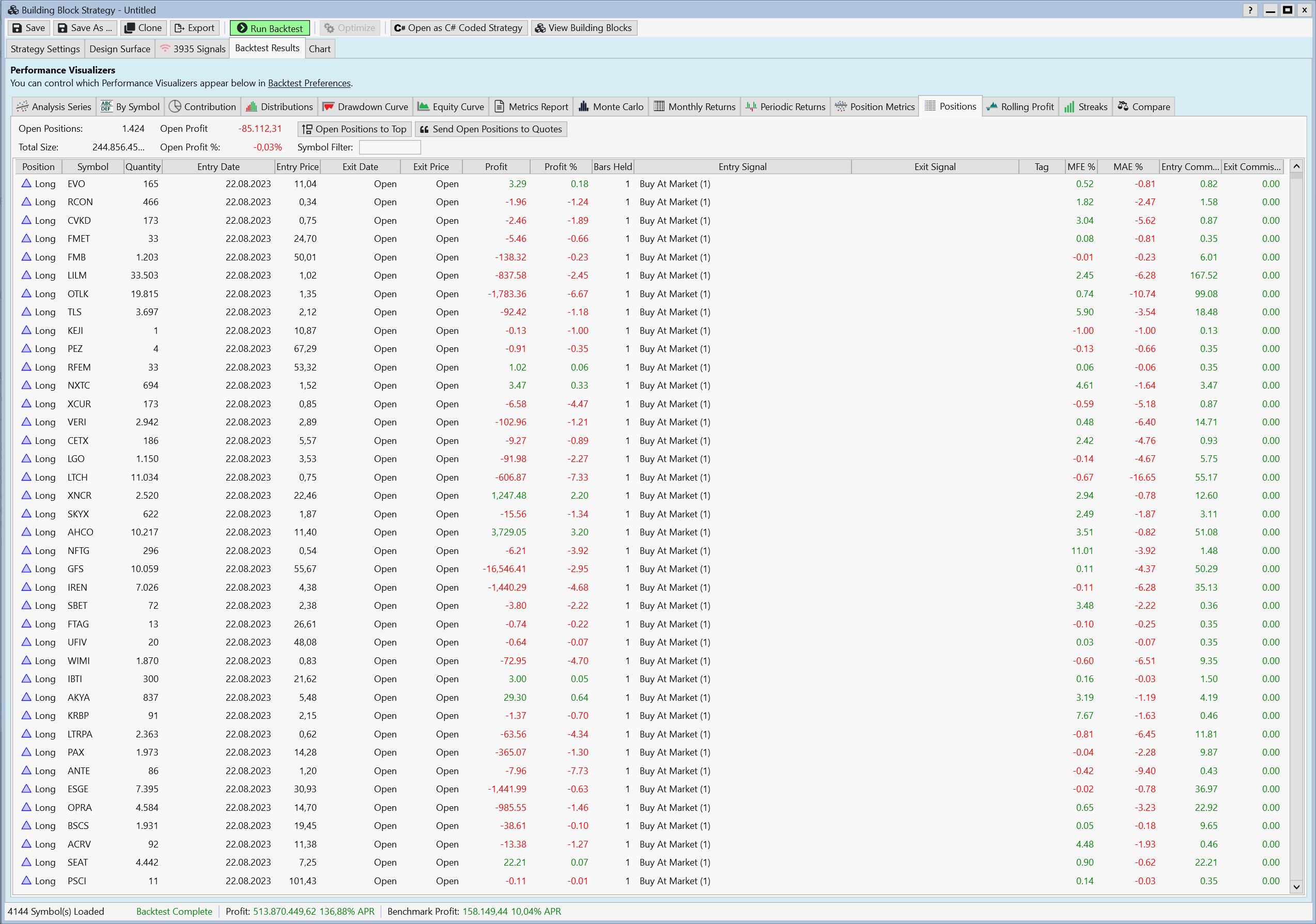

When I use bigger portfolios for backtest (i.e. Nasdaq Composite) I get very special results. In my case I use 10 % of Equity with a small margin and would expect something like 10 open positions.

The result is a large number of open positions (> 100) an the runtime is very long, even for a run with 4144 symbols).

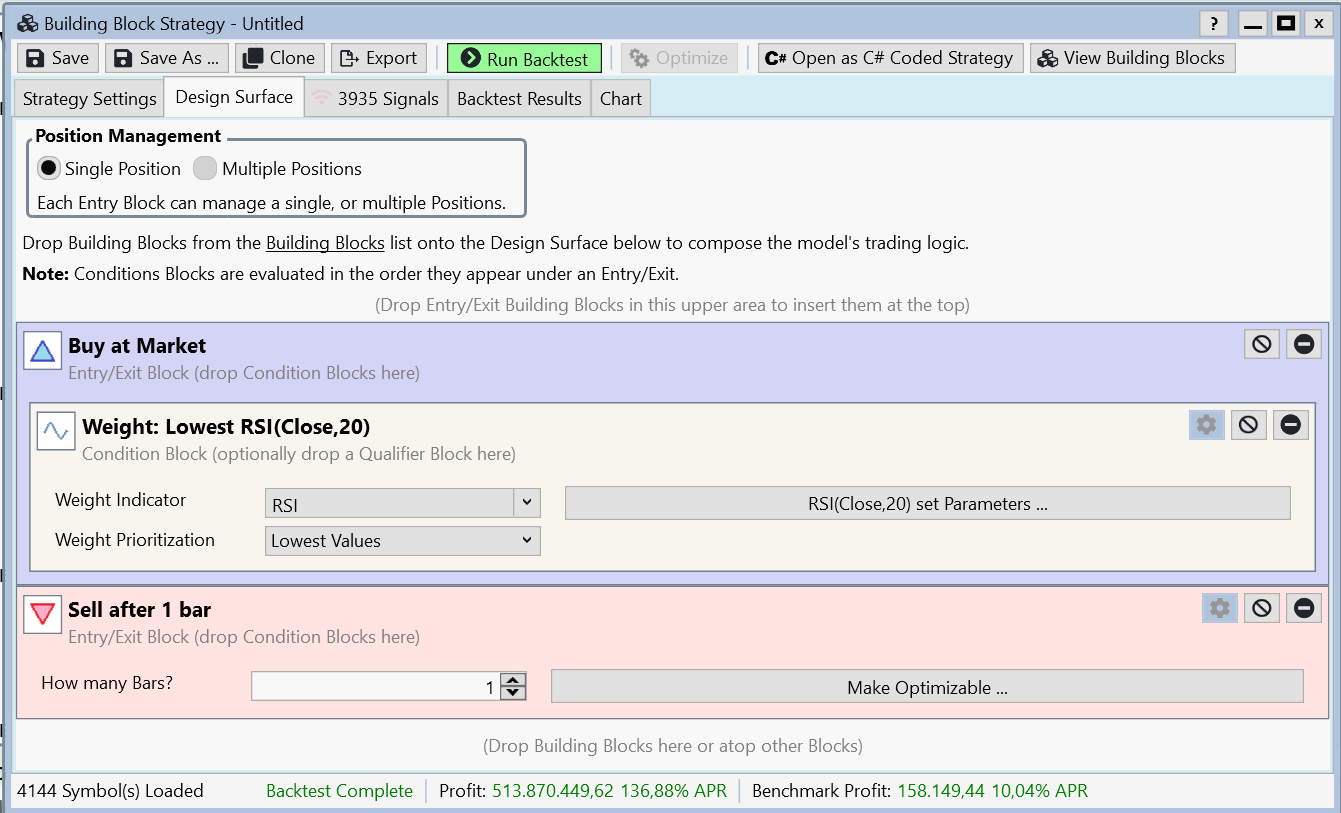

The logic for this test is extremly simple, the results are to good to be true.

All in all, for me it seems to be a bug?

The result is a large number of open positions (> 100) an the runtime is very long, even for a run with 4144 symbols).

The logic for this test is extremly simple, the results are to good to be true.

All in all, for me it seems to be a bug?

Rename

Check your backtest settings, you might have enabled a cap on the number of shares as a percent of volume.

The Volume % Limit was at 1 %. I have changed it to 0. Then the problem disappeared.

Thank you!

Thank you!

Your Response

Post

Edit Post

Login is required