I am currently trying to look at short strategies in Monte Carlo simulations.

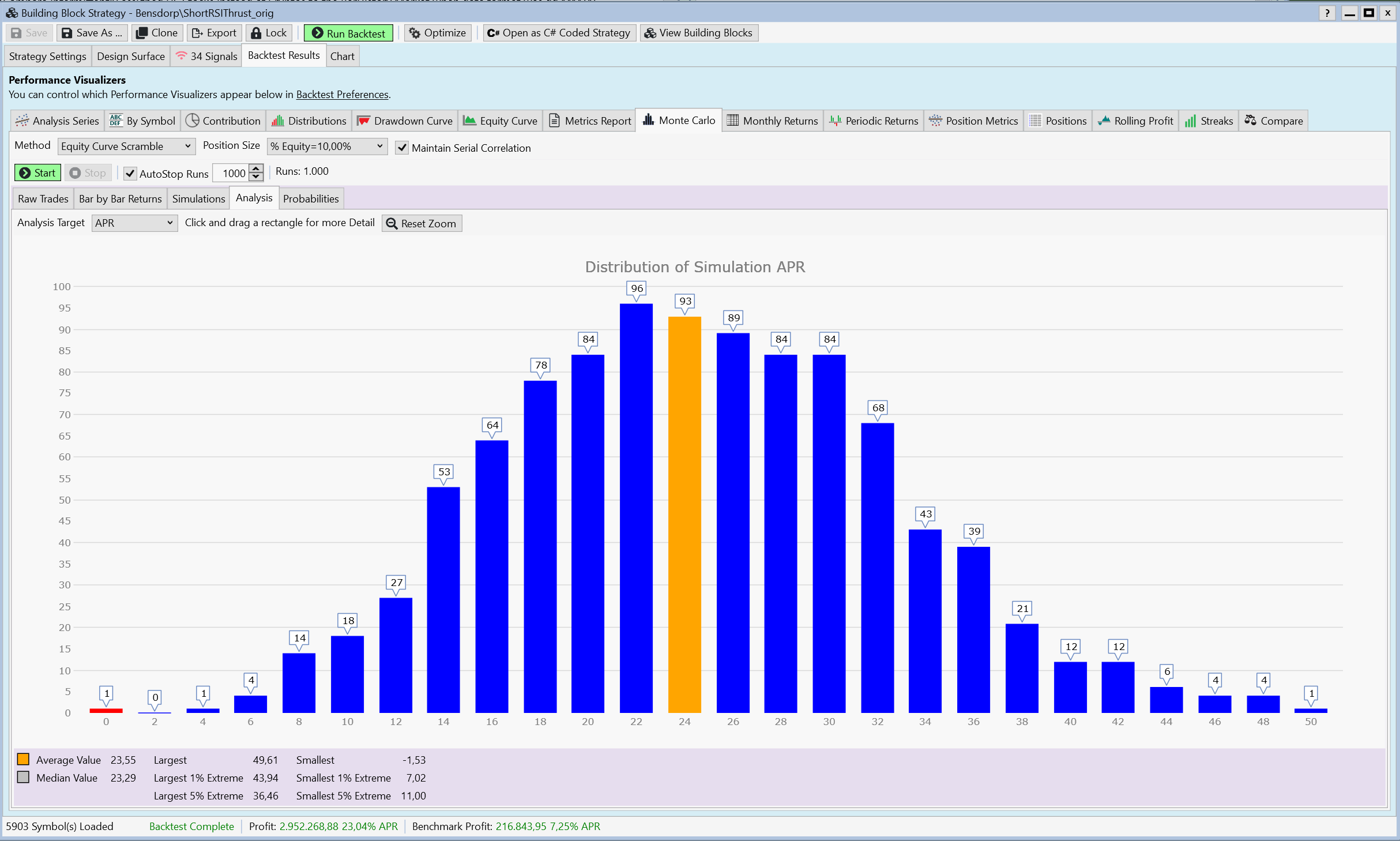

A normal backtest looks ok (e.g. Short RSI Thrust). Also with the Equity Curve Scramble method the APR looks good.

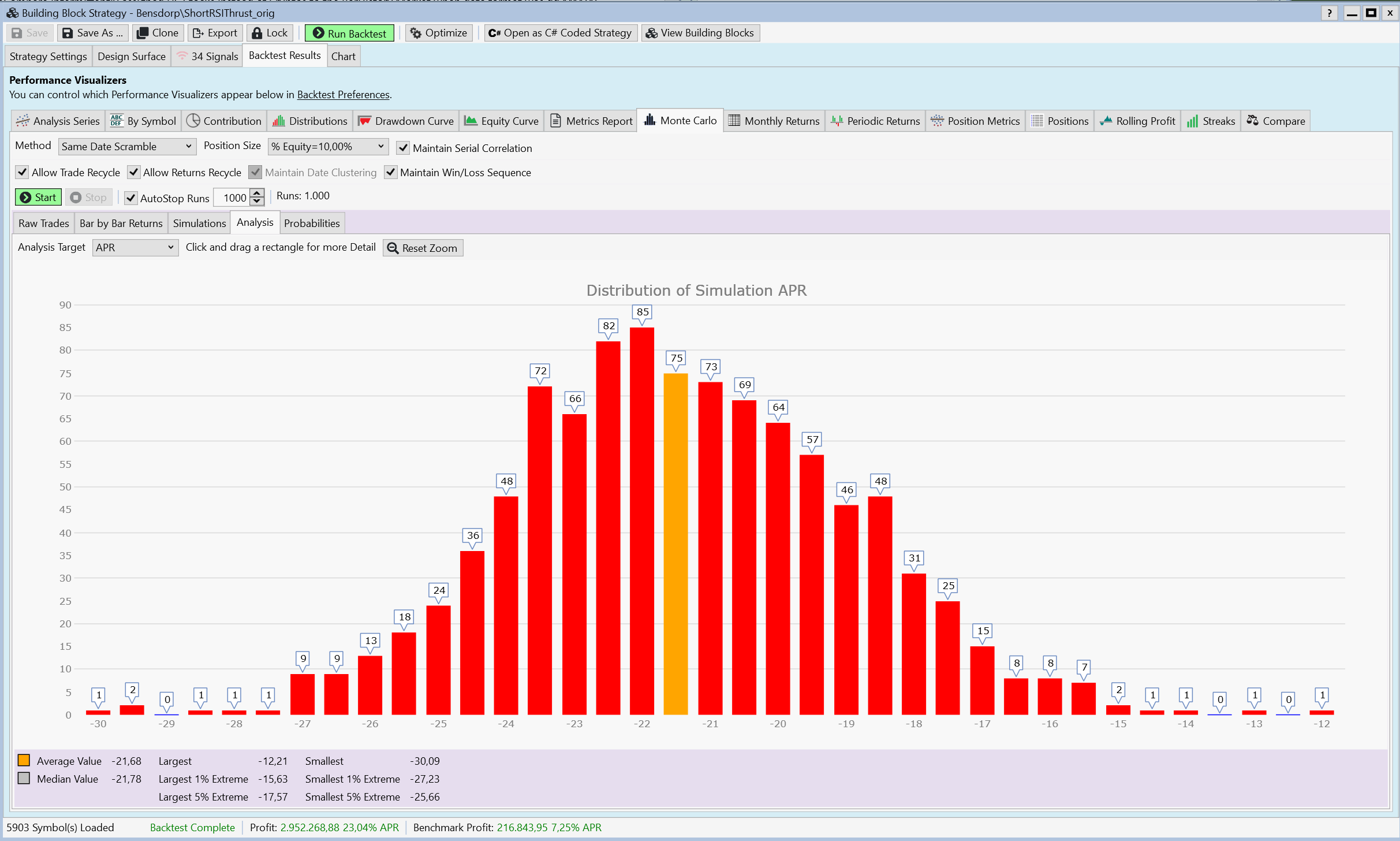

With the "Same Data Scramble" method and the other methods, there is always a negative APR.

Am I doing something wrong?

A normal backtest looks ok (e.g. Short RSI Thrust). Also with the Equity Curve Scramble method the APR looks good.

With the "Same Data Scramble" method and the other methods, there is always a negative APR.

Am I doing something wrong?

Rename

It doesn't look right. We'll investigate.

Just verified Dion's fix for this in B43.

Your Response

Post

Edit Post

Login is required