Just curious, I like to develop strategies for leveraged etf's mainly UPRO and TQQQ, but wish I had more historical data. since they were only started in 2009/2010. If someone created simulated historical data would it be possible to upload to wealth-lab?

Also per chance does anyone know of any simulated historical data out there or anyone I could pay to create it?

Also per chance does anyone know of any simulated historical data out there or anyone I could pay to create it?

Rename

I don't know of a source, but I'd also be interested in getting my hands on one! Perhaps we can reverse engineer TQQQ and simulate it going back in history?

Thats my goal glitch, I read some articles and tried it out when I was using realtest, but I couldn't get it to work well.

I've seen some people do it for Portfolio Visualizer over on the bogleheads forum, but they only calculated Daily change % and not open/close prices.

It would be awesome to see how these funds would have performed at least through the 2008 crash if not earlier.

I've seen some people do it for Portfolio Visualizer over on the bogleheads forum, but they only calculated Daily change % and not open/close prices.

It would be awesome to see how these funds would have performed at least through the 2008 crash if not earlier.

I’ve also wondered if the very existence of these funds has changed the market behavior dynamic. In 2008 it wasn’t quite as easy to go short for the average joe trader. Now anyone can buy SQQQ just like it was an ordinary stock.

Not anyone -

If you live in Europe, you cannot buy U.S. ETFs.

(Not even I can - and I'm an American with U.S. accounts living in Europe.)

If you live in Europe, you cannot buy U.S. ETFs.

(Not even I can - and I'm an American with U.S. accounts living in Europe.)

I was looking at trying to do this with the One Percent strategy since it trades on daily data (I can't find any source with less than daily timeframe before 2009ish). My thought is to use QQQ as a proxy with trade 3x margin, and change the entry/exit percentages to reflect the smaller fluctuations, but when I set the Margin Factor to 3 doesn't change the results of the run vs. a margin of 1.

Any ideas?

Any ideas?

Changing the margin factor just allows the backtest to use more margin.

If you don't increase the position size then you won't see any impact.

Maybe triple the position size as well?

If you don't increase the position size then you won't see any impact.

Maybe triple the position size as well?

Changing the position size increases the $$ return but doesn't change the % return.

What I'm hoping to see is that the backtest will incorporate the 3x margin (i.e. add $2 for each $1 in the position size) for each trade. I'm not seeing that, but I could be missing a setting or I'm mis-interpreting how the margin factor works.

What I'm hoping to see is that the backtest will incorporate the 3x margin (i.e. add $2 for each $1 in the position size) for each trade. I'm not seeing that, but I could be missing a setting or I'm mis-interpreting how the margin factor works.

I can't tell what you're looking at but the % return of each trade is not affected by sizing.

For long trades, it's always just 100 x (SellPrice / BuyPrice - 1);

But if the $$ return increases, then Profit % and APR increases, necessarily.

For long trades, it's always just 100 x (SellPrice / BuyPrice - 1);

But if the $$ return increases, then Profit % and APR increases, necessarily.

It does change the % return.

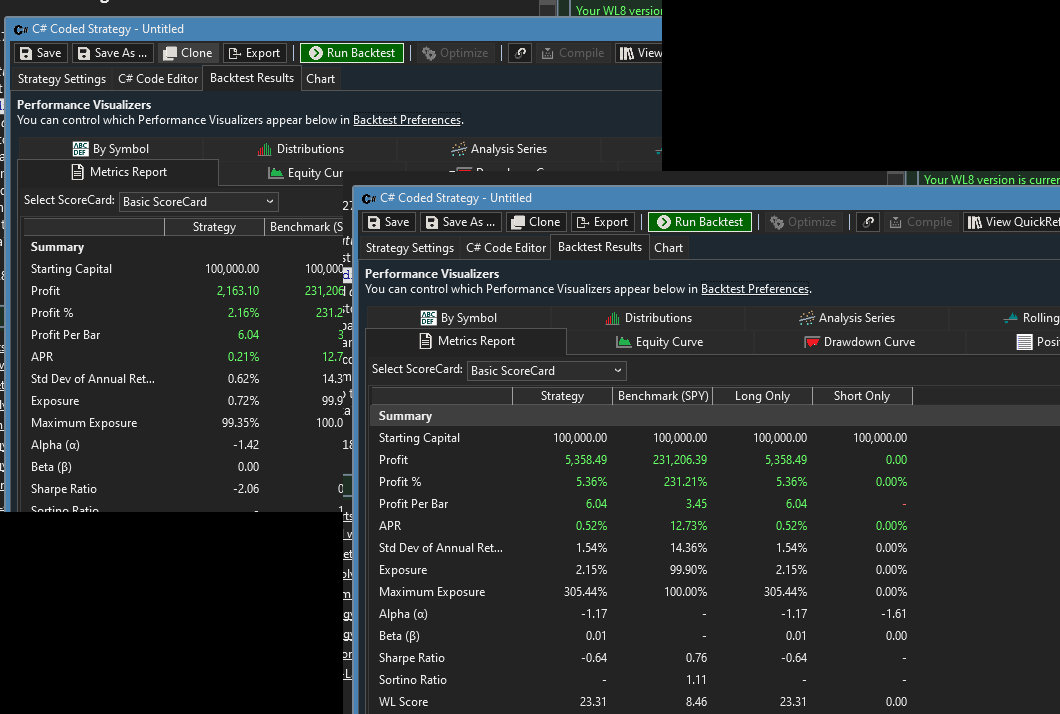

Here's proof, a simple Strategy that places and exits one trade.

If I run it on SPY with 100% of equity position sizing, Margin 1, I get profit of 2163.10 and profit % of 2.16%.

If I change the position size to 300% of equity and Margin 3, I get a profit of 5358.49 and profit % of 5.36%.

Here's proof, a simple Strategy that places and exits one trade.

CODE:

//execute the strategy rules here, this is executed once for each bar in the backtest history public override void Execute(BarHistory bars, int idx) { if (idx == bars.Count - 20) PlaceTrade(bars, TransactionType.Buy, OrderType.Market); if (idx == bars.Count - 2) PlaceTrade(bars, TransactionType.Sell, OrderType.Market); }

If I run it on SPY with 100% of equity position sizing, Margin 1, I get profit of 2163.10 and profit % of 2.16%.

If I change the position size to 300% of equity and Margin 3, I get a profit of 5358.49 and profit % of 5.36%.

Ah I see, I need to change both the margin factor and the percent of equity. That works!

Thanks.

Thanks.

You didn’t change your position size. It’s 100% of equity in each backtest. You need to change the second backtest to 300% of equity.

Thanks, Glitch, I just realized that and edited my previous entry.

Have a great weekend, thanks again for the help!

Have a great weekend, thanks again for the help!

QUOTE:

Perhaps we can reverse engineer TQQQ and simulate it going back in history?

Post #1

When attempting to simulate leveraged ETF's such as TQQQ, it's important to keep in mind that it's not as simple as multiplying an underlying value by x3 over time. The engine for these ETF's reallocates the portfolio after market close every day. This is to help insure that for a single day TQQQ will move 3x vs. the underlying. If your simulation holds TQQQ, without recalibrating each day, it will become increasingly inaccurate over time. This is because of the effect of compounding leverage over time.

Here's a hypothetical example. Let's assume that at market open NDX is at 10,000 and TQQQ is at $100. If NDX closes at 9900 that day (-1%), you would expect TQQQ to be at $97 (-3%). And the NAV for TQQQ will probably be close (although it might trade at a different price based on market demand.). If the next day QQQ closes back at $100 (+1.01%), you might expect TQQQ to return to 10,000. But it's designed to go up 3.03% which would put it at $99.94. This means that leveraged ETF's held long term can underperform their stated leverage [i]over time[/i], especially in highly volatile markets.

I believe it should be possible to synthetically create a longer TQQQ history, but the daily algorithm has to account for the way it is recalibrated each day.

Your Response

Post

Edit Post

Login is required