Need Help Converting OR building with Blocks, Thanks in advance

CODE:

//@version=4 study("Rule Number 1 Signals [ALERTS]", overlay=true) //This strategy is based off of the Book Rule #1 by Phil Town which teaches Long Term GARP/Value investing. There are three signals, MACD, Stochastics, and Moving Averages, //that are all used in conjunction to signal a LONG entry. It is better used on Daily and above time periods as the book as about long term investing. Remember, the book, //is about fundamental business analysis, to see if its a wonderful company, as the focus, and technical analysis is just a trigger. I built this as an experiment to see what //would happen if the signals were applied as per the book //MACD fastLength = input(8) slowlength = input(17) MACDLength = input(9) MACD = ema(close, fastLength) - ema(close, slowlength) aMACD = ema(MACD, MACDLength) macdDelta = MACD - aMACD //SMA signal smaSignal = input(10) sma = sma(close, smaSignal) //Stochastics 14-5 (Slow) stochasticLength = input(14, minval=1) stochasticOverBought = input(80) stochasticOverSold = input(20) smoothK = 5 smoothD = 5 k = sma(stoch(close, high, low, stochasticLength), smoothK) d = sma(k, smoothD) //Buy and close conditions smaCrossOver = crossover(close, sma) stochasticCrossOver = crossover(k, d) macdCrossOver = crossover(macdDelta, 0) smaBullish = crossover(close, sma) or close >= sma and abs(close - sma) > abs(close[1]) - sma[1] macdBullish = crossover(macdDelta, 0) or macdDelta >= 0 and abs(MACD - aMACD) > abs(MACD[1] - aMACD[1]) stochasticBullish = crossover(k, d) or k >= d and abs(k - d) > abs(k[1] - d[1]) macdCrossUnder = crossunder(macdDelta, 0) stochasticCrossUnder = crossunder(k, d) smaCrossUnder = crossunder(close, sma(close, smaSignal)) smaBearish = crossunder(close, sma) or close <= sma and abs(close - sma) > abs(close[1]) - sma[1] macdBearish = crossunder(macdDelta, 0) or macdDelta >= 0 and abs(MACD - aMACD) > abs(MACD[1] - aMACD[1]) stochasticBearish = crossunder(k, d) or k <= d and abs(k - d) > abs(k[1] - d[1]) //Set up the premises for the strategy le = macdCrossOver and smaBullish and stochasticBullish or macdBullish and smaCrossOver and stochasticBullish or macdBullish and smaBullish and stochasticCrossOver se = macdCrossUnder and smaBearish and stochasticBearish or macdBearish and smaCrossUnder and stochasticBearish or macdBearish and smaBearish and stochasticCrossUnder //Strategy to go long or to close out long term positions. // if long // strategy.entry("buy", strategy.long, 10, comment="BUY") // if closeLong // strategy.close("buy") le_filt = le and not se se_filt = se and not le prev = 0 prev := se_filt ? 1 : le_filt ? -1 : prev[1] se_final = se_filt and prev[1] == -1 le_final = le_filt and prev[1] == 1 plotshape(le_final, style=shape.arrowup, location=location.belowbar, text="buy", color=color(#fdf6e3), textcolor=color(#fdf6e3)) plotshape(se_final, style=shape.arrowdown, location=location.abovebar, text="sell" , color=(#ffa726), textcolor=color(#ffa726))

Rename

How's your evaluation going? You asked for Money Flow oscillator two months ago:

https://www.wealth-lab.com/Discussion/The-Money-Flow-Oscillator-Apirine-6267

https://www.wealth-lab.com/Discussion/The-Money-Flow-Oscillator-Apirine-6267

Hey Eugene,

I did not max my old evaluation and did not get help, I download it again to my new PC i was hopping to get help and fully evaluate this time, hope you can help me to convert this script, Thanks in advance

I did not max my old evaluation and did not get help, I download it again to my new PC i was hopping to get help and fully evaluate this time, hope you can help me to convert this script, Thanks in advance

Hi Uriel,

Our logs tell that you used the demo for two weeks straight back in May, staying pretty active almost daily.

If you like Wealth-Lab 7 kindly consider subscribing (e.g. to a monthly plan for starters) and then we can look into some custom programming. Thanks in advance.

Our logs tell that you used the demo for two weeks straight back in May, staying pretty active almost daily.

If you like Wealth-Lab 7 kindly consider subscribing (e.g. to a monthly plan for starters) and then we can look into some custom programming. Thanks in advance.

Thanks Eugene, Sure I can do that, Done!

You're welcome. Here goes your code!

CODE:

using WealthLab.Backtest; using System; using WealthLab.Core; using WealthLab.Indicators; using System.Drawing; using System.Collections.Generic; namespace WealthScript2 { public class urielted20210722 : UserStrategyBase { //create indicators and other objects here, this is executed prior to the main trading loop public override void Initialize(BarHistory bars) { //MACD int fastLength = 8, slowlength = 17, MACDLength = 9; macd = MACD.Series(bars.Close, fastLength, slowlength); aMACD = EMA.Series(macd, MACDLength); macdDelta = macd - aMACD; //SMA signal int smaSignal = 10; sma = SMA.Series(bars.Close, smaSignal); //Stochastics 14-5 (Slow) int stochasticLength = 14, stochasticOverBought = 80, stochasticOverSold = 20, smoothK = 5, smoothD = 5; k = SMA.Series(StochK.Series(bars, stochasticLength), smoothK); d = StochD.Series(bars, smoothK, smoothD); prev = new TimeSeries(bars.DateTimes, 0); PlotTimeSeriesLine(macd, "macd", "MACD", Color.Brown); PlotTimeSeriesLine(aMACD, "macd signal", "MACD", Color.DarkGreen); PlotTimeSeries(macdDelta, "macd delta", "MACD", Color.Blue, PlotStyles.ThickHistogram); PlotTimeSeriesLine(sma, "sma", "Price", Color.Blue); PlotTimeSeriesLine(k, "stochK", "Stoch", Color.Red); PlotTimeSeriesLine(d, "stochD", "Stoch", Color.Blue); } //execute the strategy rules here, this is executed once for each bar in the backtest history public override void Execute(BarHistory bars, int idx) { if (idx > 0) { //Buy and close conditions bool smaCrossOver = bars.Close.CrossesOver(sma, idx); bool stochasticCrossOver = k.CrossesOver(d, idx); bool macdCrossOver = macdDelta.CrossesOver(0, idx); bool smaBullish = smaCrossOver || (bars.Close[idx] >= sma[idx] && Math.Abs(bars.Close[idx] - sma[idx]) > Math.Abs(bars.Close[idx - 1] - sma[idx - 1])); bool macdBullish = macdCrossOver || macdDelta[idx] >= 0 && Math.Abs(macdDelta[idx]) > Math.Abs(macdDelta[idx - 1]); bool stochasticBullish = stochasticCrossOver || k[idx] >= d[idx] && Math.Abs(k[idx] -d[idx]) > Math.Abs(k[idx - 1] - d[idx - 1]); bool smaCrossUnder = bars.Close.CrossesUnder(sma, idx); bool macdCrossUnder = macdDelta.CrossesUnder(0, idx); bool stochasticCrossUnder = k.CrossesUnder(d, idx); bool smaBearish = smaCrossUnder || (bars.Close[idx] <= sma[idx] && Math.Abs(bars.Close[idx] - sma[idx]) > Math.Abs(bars.Close[idx - 1] - sma[idx - 1])); bool macdBearish = macdCrossUnder || macdDelta[idx] >= 0 && Math.Abs(macdDelta[idx]) > Math.Abs(macdDelta[idx - 1]); bool stochasticBearish = stochasticCrossUnder || k[idx] <= d[idx] && Math.Abs(k[idx] -d[idx]) > Math.Abs(k[idx - 1] - d[idx - 1]); //Set up the premises for the strategy bool le = (macdCrossOver && smaBullish && stochasticBullish) || (macdBullish && smaCrossOver && stochasticBullish) || (macdBullish && smaBullish && stochasticCrossOver); bool se = (macdCrossUnder && smaBearish && stochasticBearish) || (macdBearish && smaCrossUnder && stochasticBearish) || (macdBearish && smaBearish && stochasticCrossUnder); bool le_filt = le && !se; bool se_filt = se && !le; if(idx > 0) prev[idx] = se_filt ? 1 : le_filt ? -1 : prev[idx -1]; else prev[idx] = 0; bool se_final = idx > 0 ? se_filt && prev[idx -1] == -1 : false; bool le_final = idx > 0 ? le_filt && prev[idx -1] == 1 : false; if (!HasOpenPosition(bars, PositionType.Long)) { //code your buy conditions here if(le_final) PlaceTrade(bars, TransactionType.Buy, OrderType.Market); } else { //code your sell conditions here if(se_final) PlaceTrade(bars, TransactionType.Sell, OrderType.Market); } } } //declare private variables below TimeSeries macd, aMACD, macdDelta, k, d, sma, prev; } }

Thank you

Eugene,

The strategy build on Rule#1 book the info for the strategy layout here:

http://docshare04.docshare.tips/files/26904/269043119.pdf

Please advice if the code match setting

Thanks in advance

The strategy build on Rule#1 book the info for the strategy layout here:

http://docshare04.docshare.tips/files/26904/269043119.pdf

Please advice if the code match setting

Thanks in advance

Buy methodology in regards to the Three Tools:

1. Latest closing price above 30- period moving average;

2. %K line of slow stochastic oscillator above %D line; and

3. MACD histogram above centerline (greater than zero).

Sell rules in regards to the Three Tools are:

1. %K line of slow stochastic falls below %D line; and

2. MACD histogram falls below centerline (is less than zero);

and

3. The stock is trading sideways.

Three Greens You’re In, Two

Reds You’re Out

1. Latest closing price above 30- period moving average;

2. %K line of slow stochastic oscillator above %D line; and

3. MACD histogram above centerline (greater than zero).

Sell rules in regards to the Three Tools are:

1. %K line of slow stochastic falls below %D line; and

2. MACD histogram falls below centerline (is less than zero);

and

3. The stock is trading sideways.

Three Greens You’re In, Two

Reds You’re Out

The script contains a lot more logic that your rules in Post #8. I've provided a literal translation of the script in #1.

Eugene,

Can this be build with blocks ?

Can this be build with blocks ?

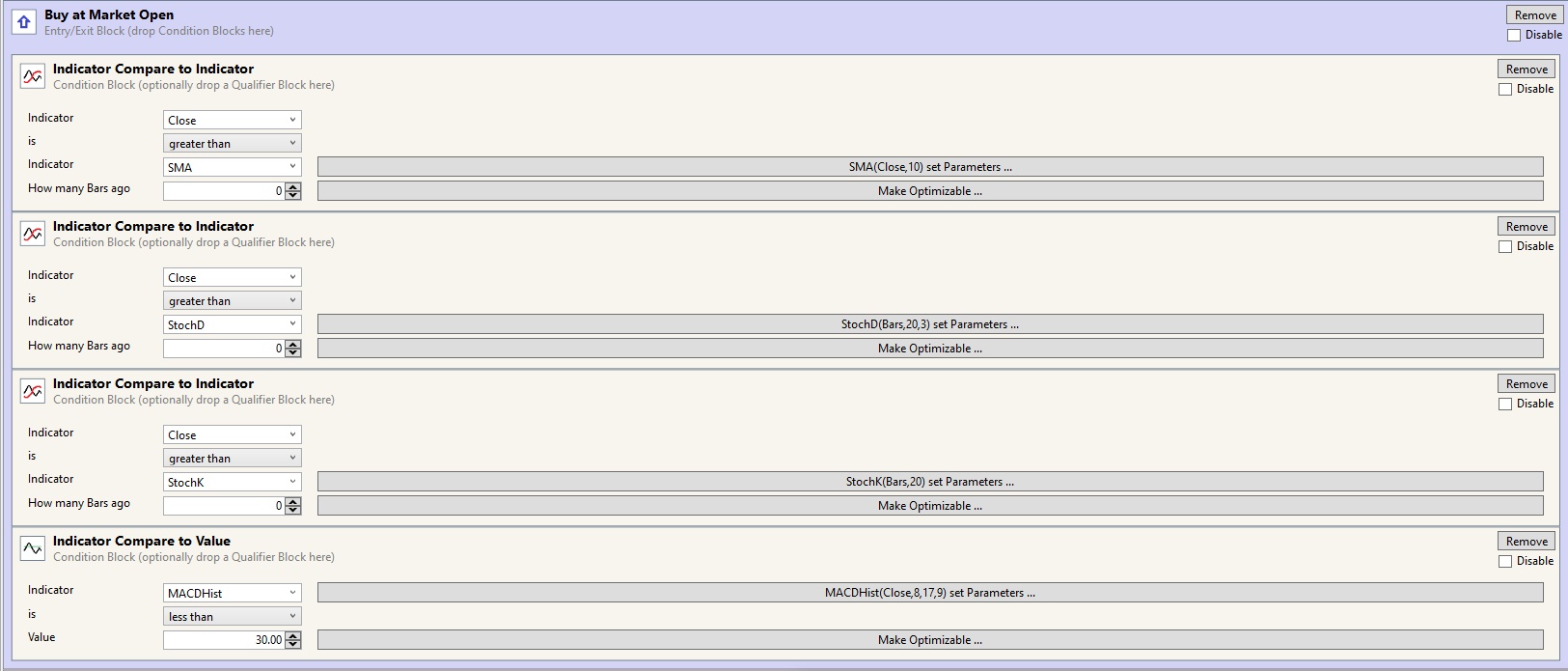

Uriel, it's unlikely that the logic in #1 could be programmed in Blocks. However, the rules in Post #8 can certainly be:

Buy rules:

1. Latest closing price above 30- period moving average; => Use "Indicator Compare to Indicator", Close and SMA

2. %K line of slow stochastic oscillator above %D line; and => Use "Indicator Compare to Indicator", StochK and StochD

3. MACD histtogram above centerline (greater than zero). => Use "Indicator Compare to Value", MACDHist

Sell rules in regards

1. %K line of slow stochastic falls below %D line; and => Use "Indicator Compare to Indicator", StochK and StochD

2. MACD histogram falls below centerline (is less than zero); => Use "Indicator Compare to Value", MACDHist

3. The stock is trading sideways. => Use "Indicator Compare to Value", ADX < 25

* Helpful resources:

https://wl6.wealth-lab.com/Forum/Posts/Rules-WL6-gt-Building-Blocks-WL7-40617/

https://www.wealth-lab.com/Discussion/Quick-WL6-9-to-WL7-Translation-Guide-5548

Buy rules:

1. Latest closing price above 30- period moving average; => Use "Indicator Compare to Indicator", Close and SMA

2. %K line of slow stochastic oscillator above %D line; and => Use "Indicator Compare to Indicator", StochK and StochD

3. MACD histtogram above centerline (greater than zero). => Use "Indicator Compare to Value", MACDHist

Sell rules in regards

1. %K line of slow stochastic falls below %D line; and => Use "Indicator Compare to Indicator", StochK and StochD

2. MACD histogram falls below centerline (is less than zero); => Use "Indicator Compare to Value", MACDHist

3. The stock is trading sideways. => Use "Indicator Compare to Value", ADX < 25

* Helpful resources:

https://wl6.wealth-lab.com/Forum/Posts/Rules-WL6-gt-Building-Blocks-WL7-40617/

https://www.wealth-lab.com/Discussion/Quick-WL6-9-to-WL7-Translation-Guide-5548

Please advice the correct setting: image attach

Your Response

Post

Edit Post

Login is required