Hello, a question about MetaStrategie Settings.

I have two strategies with an APR over 30% and over 5000 trades per strategy.

With the MetaStrategy I get a result of APR 20% and 1500 trades are evaluated as a result.

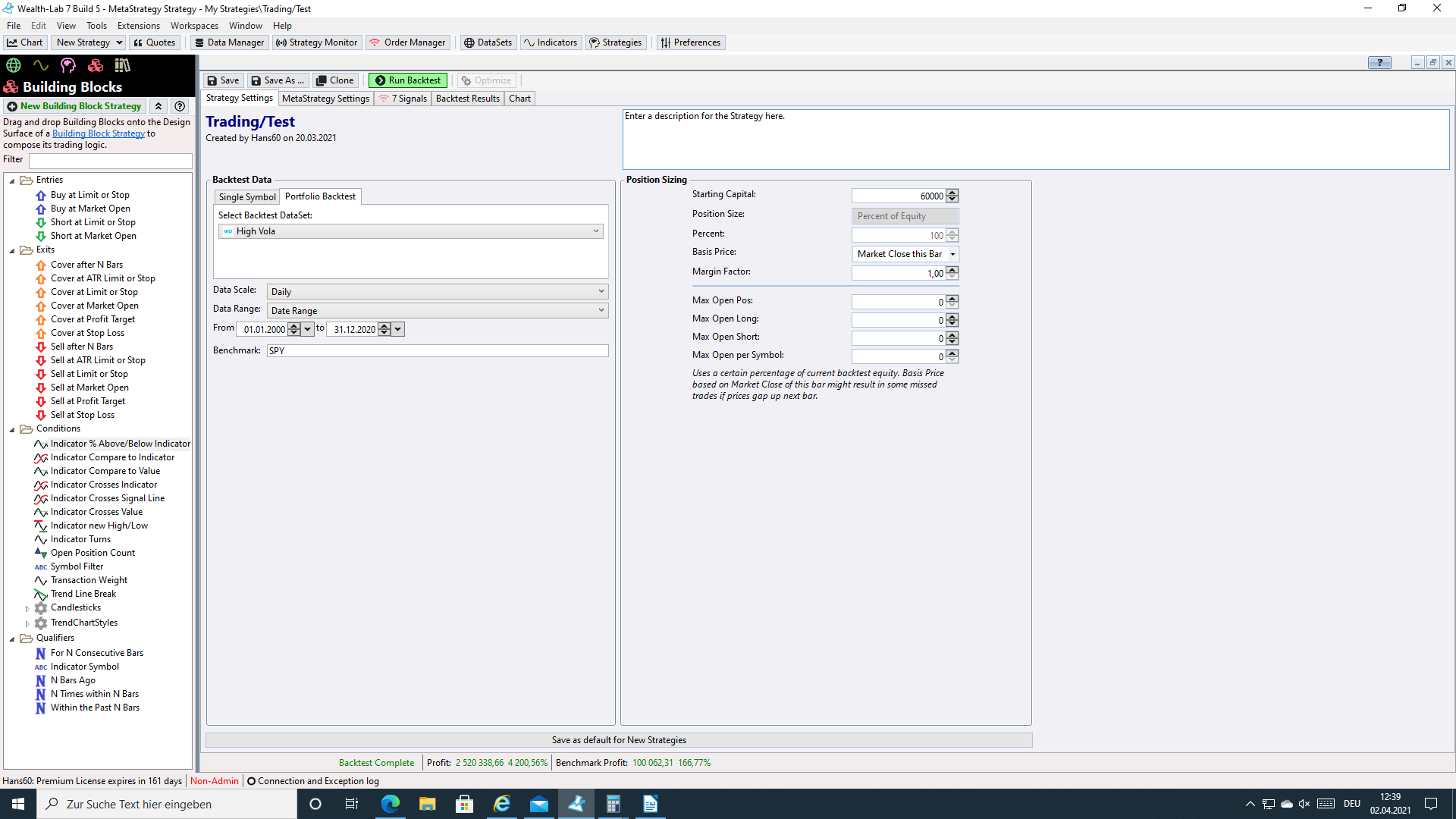

Distribution of the capital is 50%.

I doubled the capital with the MetaStrategy so that the respective strategy has the same initial capital as with the individual backtest.

For my understanding, a result close to APR should actually be 30% and the number of trades at least 10,000.

Best regards

Hans

I have two strategies with an APR over 30% and over 5000 trades per strategy.

With the MetaStrategy I get a result of APR 20% and 1500 trades are evaluated as a result.

Distribution of the capital is 50%.

I doubled the capital with the MetaStrategy so that the respective strategy has the same initial capital as with the individual backtest.

For my understanding, a result close to APR should actually be 30% and the number of trades at least 10,000.

Best regards

Hans

Rename

You are comparing a strategy backtest with 100% equity per position with a MetaStrategy where it has 14% equity assigned. Why would you expect a parity of results?

I have now seen that the holding period does not fit either.

I have an average holding period of 7 days for the individual strategies.

At MetaStratgy, an average of 26 days.

It could now be that it is an attitude problem.

Because at the beginning I have the full number of trades and then towards the end of the test period there are fewer and fewer except for 3. The exposure is mostly at 80%.

I want to execute a maximum of 7 trades per strategy at the same time.

Here I now have a problem of understanding on my part regarding the settings

I have an average holding period of 7 days for the individual strategies.

At MetaStratgy, an average of 26 days.

It could now be that it is an attitude problem.

Because at the beginning I have the full number of trades and then towards the end of the test period there are fewer and fewer except for 3. The exposure is mostly at 80%.

I want to execute a maximum of 7 trades per strategy at the same time.

Here I now have a problem of understanding on my part regarding the settings

I stand corrected, thought it's a comparison but the three screenshots all belong to the MetaStrategy.

Right, all 3 screenshots are from MetaStrategy.

That's why I don't understand the different results.

That's why I don't understand the different results.

1. I would start by double checking the position sizing and data loading settings between the two distinct strategies and making sure they're equal - and that NSF Position count = 0 for both.

2. Important: if you run a Strategy and the backtest results change on each run, you have to assign Transaction.Weight (in code) or use the Transaction Weight condition (for Blocks).

Provided these conditions are met the results have a 100% match for me between Strategy and the corresponding MetaStrategy.

2. Important: if you run a Strategy and the backtest results change on each run, you have to assign Transaction.Weight (in code) or use the Transaction Weight condition (for Blocks).

Provided these conditions are met the results have a 100% match for me between Strategy and the corresponding MetaStrategy.

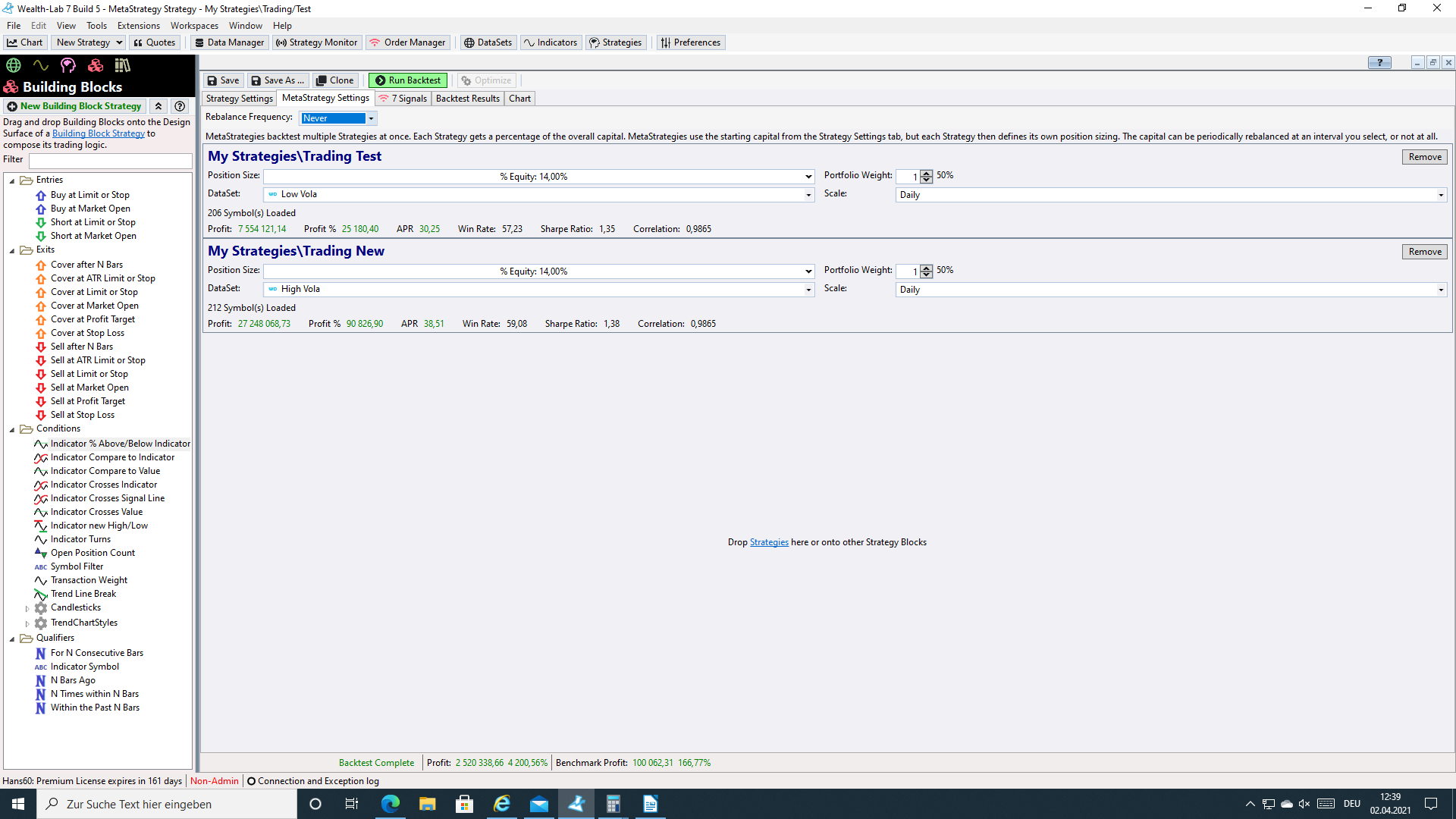

The results in the MetaStrategy Settings tab also have the same APR as for the individual strategies.

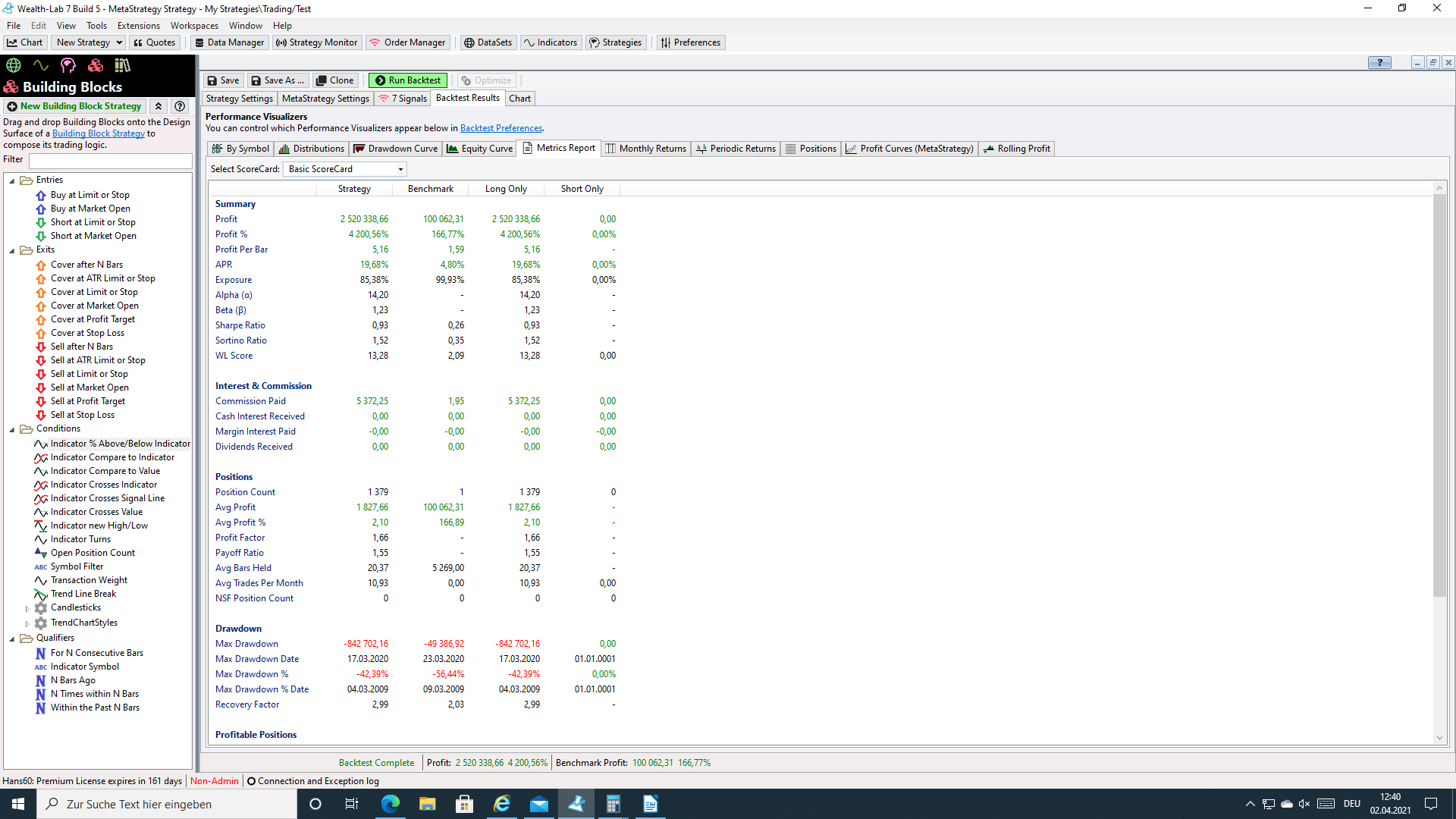

But on the Backtest Resuts tab, the key figures are very different from the key figures of the individual strategies.

The number of trades alone cannot be right.

I have over 5000 trades per strategy, that is over 10,000 in total.

But here only 1,379 appear as executed trades.

I actually wanted to test the weighting of the capital and then check the key figures.

With the Combi from WL6, the results are clearly understandable.

The number of trades is also realistic there.

But on the Backtest Resuts tab, the key figures are very different from the key figures of the individual strategies.

The number of trades alone cannot be right.

I have over 5000 trades per strategy, that is over 10,000 in total.

But here only 1,379 appear as executed trades.

I actually wanted to test the weighting of the capital and then check the key figures.

With the Combi from WL6, the results are clearly understandable.

The number of trades is also realistic there.

Please see Post #5 and follow suggestions.

I did everything as described in post 5.

Take a look at the screenshot with the MetaStrategy tab.

It shows a profit of 7 and 27 million.

That is also the result of the individual strategies.

A profit of 2.5 million on the Backtest Results tab.

Have you looked at your Backtest Results tab and the APR and the number of position counts fit if you add both strategies together?

Take a look at the screenshot with the MetaStrategy tab.

It shows a profit of 7 and 27 million.

That is also the result of the individual strategies.

A profit of 2.5 million on the Backtest Results tab.

Have you looked at your Backtest Results tab and the APR and the number of position counts fit if you add both strategies together?

QUOTE:

and the number of position counts fit if you add both strategies together?

Maybe I don't follow what you're saying but why would the number of positions be equal to the summed up value of two systems combined by a MetaStrategy? This results in a new backtest with a new portfolio equity.

With my strategies I am invested a maximum of 7 days.

Both strategies are adopted 1 to 1 in the MetaStrategy.

That actually means I cannot be invested for more than 7 days.

2 new screenshots:

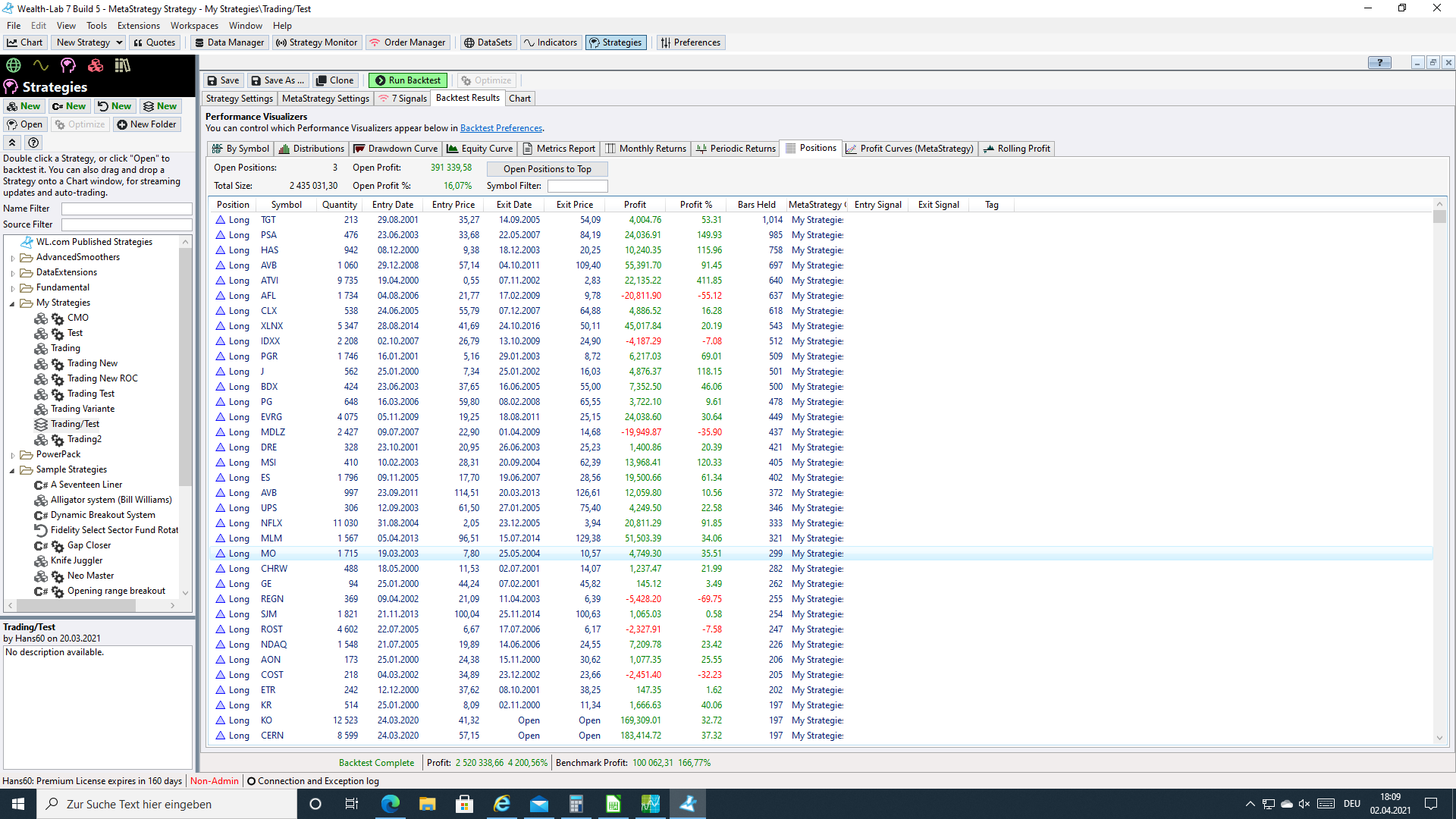

Now take a look at Bars Held, there are several 3-digit Bars Held.

Average Bars Held - Profitable 26 days, unprofitable 12 days.

Both strategies are adopted 1 to 1 in the MetaStrategy.

That actually means I cannot be invested for more than 7 days.

2 new screenshots:

Now take a look at Bars Held, there are several 3-digit Bars Held.

Average Bars Held - Profitable 26 days, unprofitable 12 days.

OK how can I reproduce this?

1) Produce 2 strategies with a fixed exit. (Sell after N bars).

2) Then merge in the MetaStrategy.

3) Check values in the Backtest Results - Positions

4) In the BarsHeld column, the maximum number of Sell after N bars must not be exceeded.

I hope the explanation is understandable.

2) Then merge in the MetaStrategy.

3) Check values in the Backtest Results - Positions

4) In the BarsHeld column, the maximum number of Sell after N bars must not be exceeded.

I hope the explanation is understandable.

I did it once and the maximum number of bars held is not exceeded. Suspecting there may be an issue with the strategy. To double check, can you 1) re-create your strategies from Blocks and 2) add them to a new MetaStrategy?

I made a very simple strategy.

And I have those high BarsHeld values again.

I have no idea what's not working here, I can't think of anything anymore.

I would love to demonstrate it live.

And I have those high BarsHeld values again.

I have no idea what's not working here, I can't think of anything anymore.

I would love to demonstrate it live.

I see what's involved here. In Wealth-Lab's Preferences > Backtest, you have NSF Positions cleared (unchecked). Once it's activated (enabled) your Bars Held will not be exceeded by the MetaStrategy.

@Glitch

Dion, do you think this behavior is expected?

@Glitch

Dion, do you think this behavior is expected?

Clearly not, right? It's actually adding NSF positions to the backtest and that should never be the case.

Perfect.

I have activated the NSF tick and the number of BarsHeld is not exceeded.

I have one more question about the NSF position.

With which setting should you perform the backtests?

I understood the difference in the result, but not yet understood the logic.

I transferred a strategy from WL6.

With NSF the results are almost the same.

Without NSF, I have a major difference.

That's why I don't know exactly which setting should be used to test or implement a strategy in the end.

I have activated the NSF tick and the number of BarsHeld is not exceeded.

I have one more question about the NSF position.

With which setting should you perform the backtests?

I understood the difference in the result, but not yet understood the logic.

I transferred a strategy from WL6.

With NSF the results are almost the same.

Without NSF, I have a major difference.

That's why I don't know exactly which setting should be used to test or implement a strategy in the end.

Hans, this MetaStrategy bug is fixed. Please look forward to Build 7 with the fix. Thanks for the heads-up.

QUOTE:There's not a right or wrong answer, but there's a difference (described in Help) and therefore it's a preference. As you found, Wealth-Lab 6's Portfolio backtest behavior "retained NSF Positions" - although this was a result of the non-optional raw profit backtest engine collecting positions for the Position sizing post-processing.

With which setting should you perform the backtests?

That said, MetaStrategies will always run with NSF Positions Retained starting with Build 7.

Your Response

Post

Edit Post

Login is required