Hi,

Is it possible to create the following system with the Building Blocks?

Thanks in advance for a support.

Buy when the close is below the 20-day moving average of the closes minus the 20-day average true range multiplied by 2.5.

Sell when the opposite is true.

Buy = Close < MA(Close,20) - (ATR(20)*2.5)

Sell = Close > MA(Close,20) + (ATR(20) * 2.5)

Is it possible to create the following system with the Building Blocks?

Thanks in advance for a support.

Buy when the close is below the 20-day moving average of the closes minus the 20-day average true range multiplied by 2.5.

Sell when the opposite is true.

Buy = Close < MA(Close,20) - (ATR(20)*2.5)

Sell = Close > MA(Close,20) + (ATR(20) * 2.5)

Rename

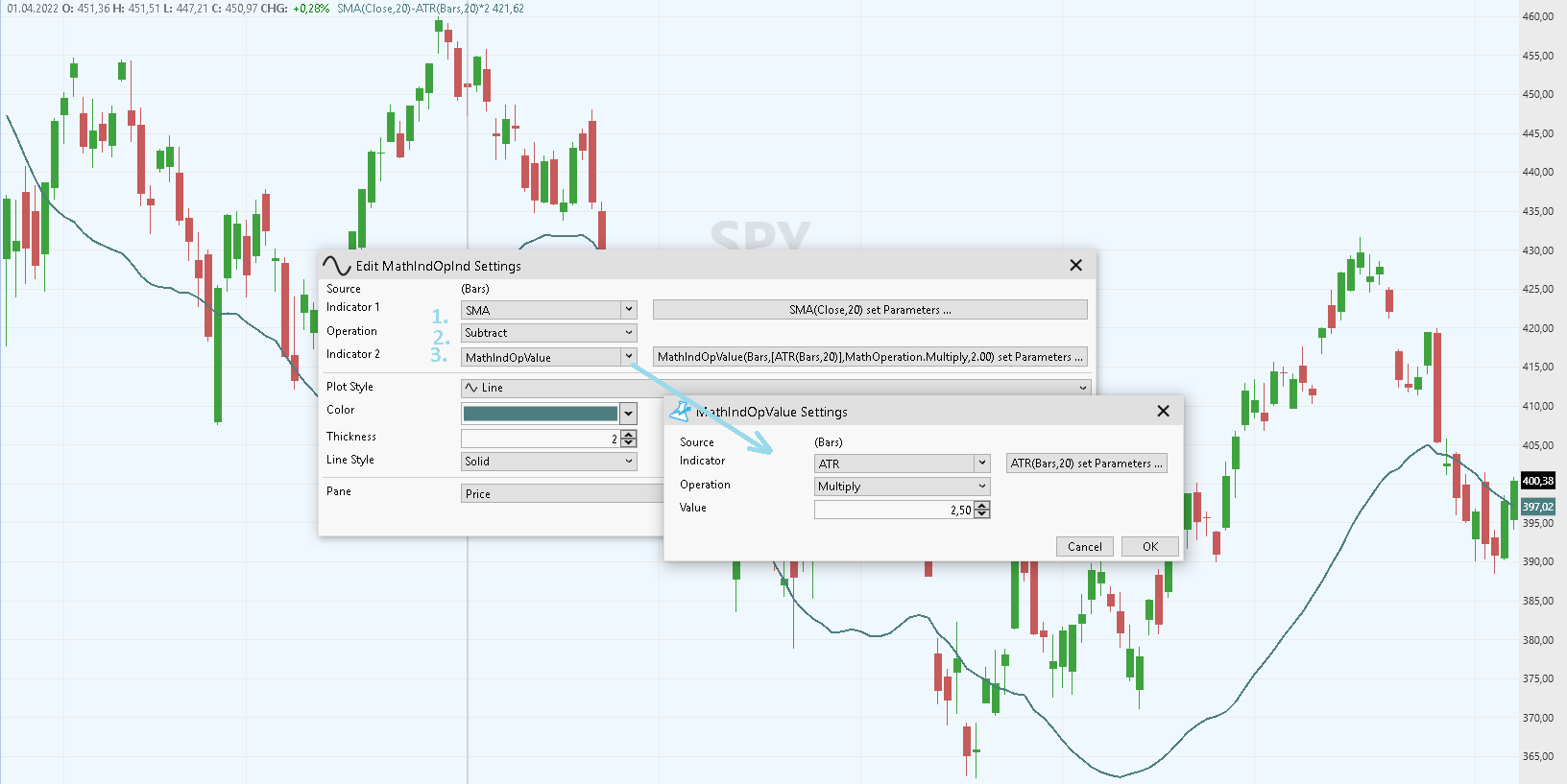

Yes, it's possible. You're looking for MathIndOp* indicators from the Transformers group. For the Buy side, it should be set up like this:

I leave the Sell side for you to construct, it's simple once you get a handle on this.

P.S. To summarize your question clearly, changed the topic title:

WAS: Question about the building blocks

IS: Buy when Close is above MA +/- ATR factor in Blocks?

I leave the Sell side for you to construct, it's simple once you get a handle on this.

P.S. To summarize your question clearly, changed the topic title:

WAS: Question about the building blocks

IS: Buy when Close is above MA +/- ATR factor in Blocks?

perfect help, THANK YOU!

:-)

:-)

hi eugene,

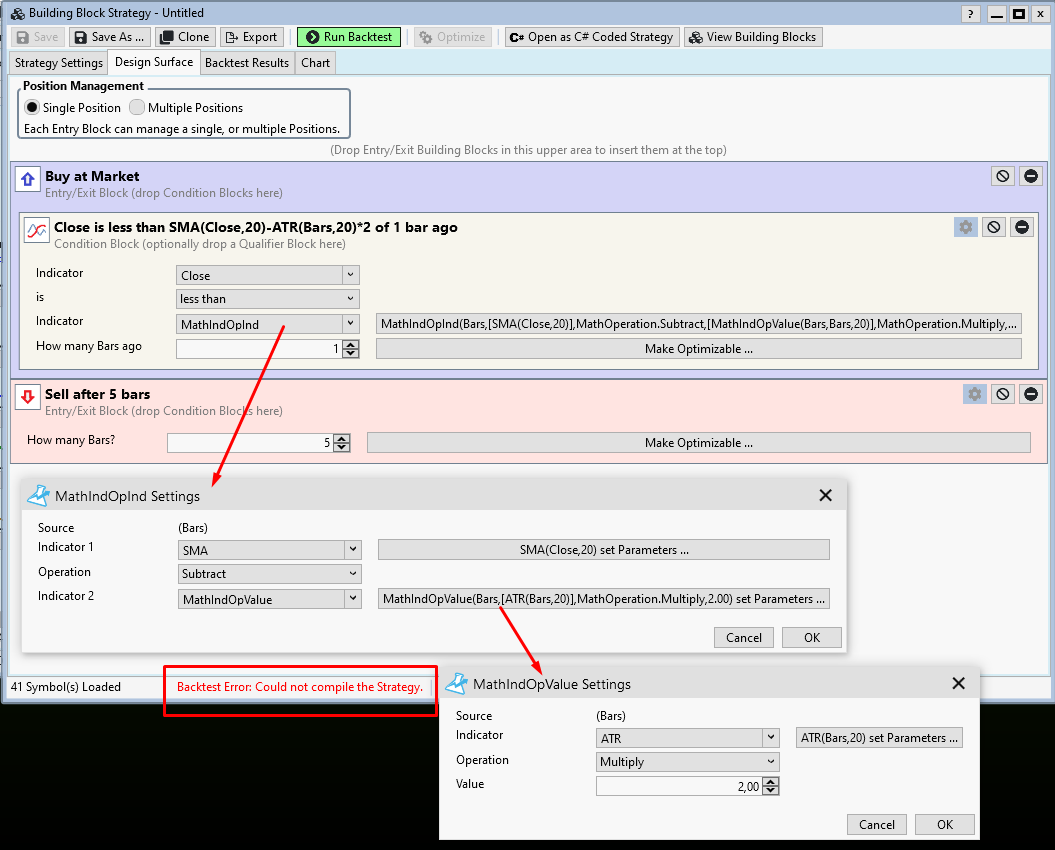

another additional question: what am I doing wrong, since your solution gives an error message.

Thanks for the support!

another additional question: what am I doing wrong, since your solution gives an error message.

Thanks for the support!

This is a current limitation with the Transformers - you can't put a Transformer in a Transformer.

The way to solve it is to create a Custom Indicator.. for the ATR multiple for example.

Then you can just use it where required.

See the Help (F1) for Indicators > Custom Indicators. If you need help, just let us know.

The way to solve it is to create a Custom Indicator.. for the ATR multiple for example.

Then you can just use it where required.

See the Help (F1) for Indicators > Custom Indicators. If you need help, just let us know.

If you're willing to use C# code then it becomes trivial - with the help of the ATRBand* indicator. It cannot be used this way in Blocks. Check this out:

CODE:

using WealthLab.Backtest; using System; using WealthLab.Core; using WealthLab.Indicators; using System.Collections.Generic; namespace WealthScript1 { public class MyStrategy : UserStrategyBase { IndicatorBase dsU, dsL; //create indicators and other objects here, this is executed prior to the main trading loop public override void Initialize(BarHistory bars) { var sma = SMA.Series(bars.Close, 20); dsU = ATRBandUpper.Series(bars, sma, 20, 2.5); dsL = ATRBandLower.Series(bars, sma, 20, 2.5); PlotIndicatorBands(dsU, dsL); } //execute the strategy rules here, this is executed once for each bar in the backtest history public override void Execute(BarHistory bars, int idx) { if (!HasOpenPosition(bars, PositionType.Long)) { //code your buy conditions here //Buy = Close < MA(Close, 20) - (ATR(20) *2.5) PlaceTrade(bars, TransactionType.Buy, OrderType.Limit, dsL[idx]); } else { //code your sell conditions here //Sell = Close > MA(Close, 20) + (ATR(20) * 2.5) PlaceTrade(bars, TransactionType.Sell, OrderType.Limit, dsU[idx]); } } //declare private variables below } }

Your Response

Post

Edit Post

Login is required