Same backtest setup - 400 crypto symbols, 1 hour timeframe, Last 10 years of data

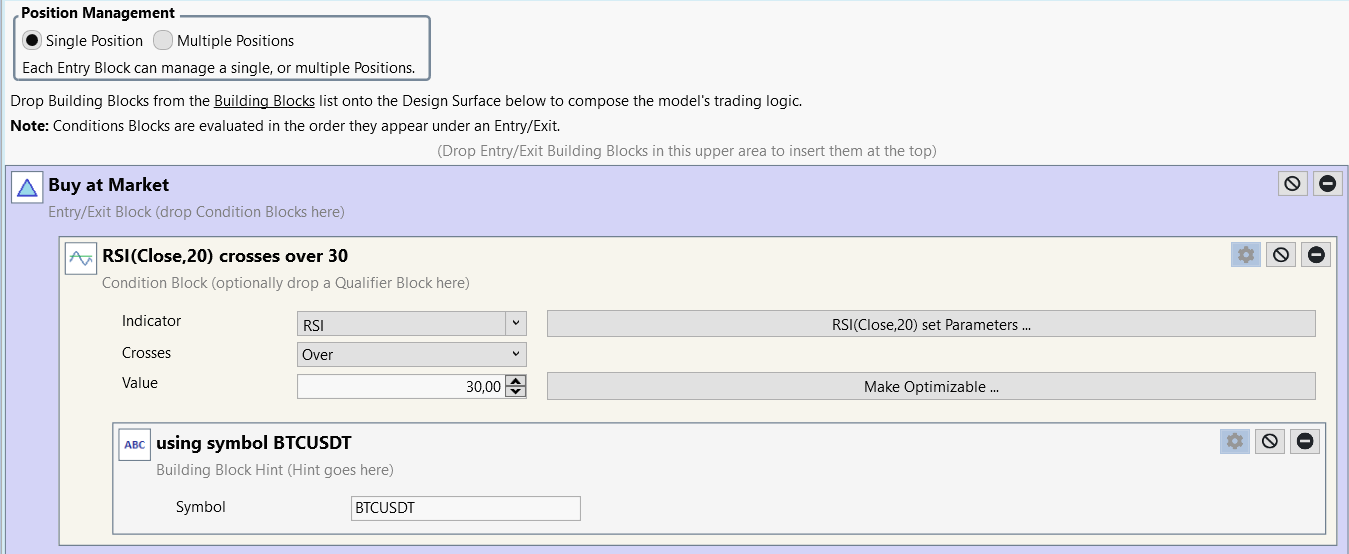

First strategy

Backtest time - 22 sec

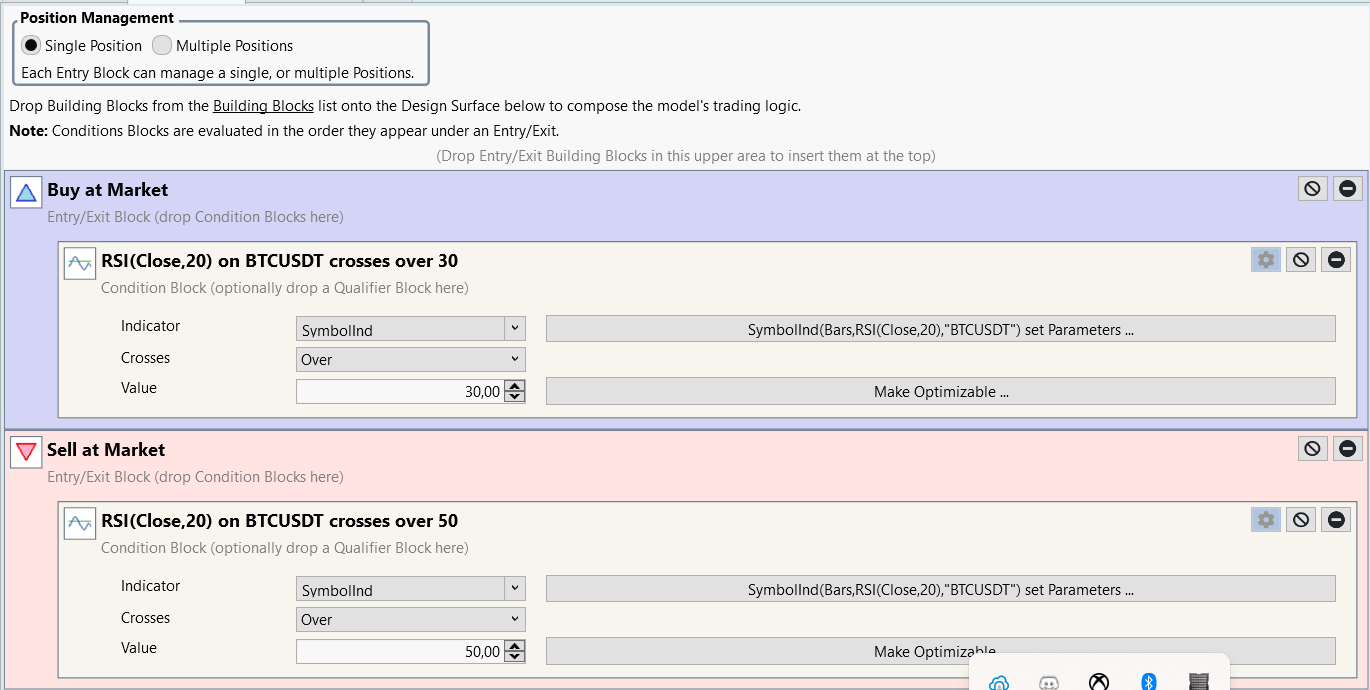

Second strategy

Backtest time - 21 min

First strategy

Backtest time - 22 sec

Second strategy

Backtest time - 21 min

Rename

I'm certainly not seeing that, here is a video of my experiencing, using the Dow 30 in both backtests,

https://drive.google.com/file/d/1nWUL-bn3uGgVl1sZXmc37UGt_UDRpvsO/view?usp=sharing

Are you sure you had all of the data completely up to date before the runs in order to make a fair test?

https://drive.google.com/file/d/1nWUL-bn3uGgVl1sZXmc37UGt_UDRpvsO/view?usp=sharing

Are you sure you had all of the data completely up to date before the runs in order to make a fair test?

Maybe 30 Symbols and dayly scale is not enough to produce huge 21 minute "Running Backtest..." lag. What I think is happening that in my first case RSI(Close,20) for BTC is calculated once and than cashed version used for each symbol in data set. In second case (whitch uses SymbolInd) indicator RSI(Close,20) for BTC is calculated for each of my 400 symbols in dataset at start of backtest and produces huge lag at start (possibly it even tryes to update the data for BTCUSDT 400 times).

QUOTE:

Are you sure you had all of the data completely up to date before the runs in order to make a fair test?

100% percent sure

It's not cached though, if you open the C# Code for the Strategy you'll see it's created each time via a "new" call. But I'll dig in and see if there's anything we can do to optimize the SymbolInd!

I think I found the cause and will work on some optimization for SymbolInd.

QUOTE:

I think I found the cause and will work on some optimization for SymbolInd.

Thank you very mutch! Looking forward to updates!

Your Response

Post

Edit Post

Login is required