Strategy is below,

1) Backtest Data

- Backtest data : DOW30

- Data scale : Daily

- Data range : 2012-09-10 ~ 2022-09-07

- Benchmark : QQQ

2) Position Sizing

- Starting Capital : 100000

- Size : Percent of Equity

- Percent : 20

- Basis Price : Market Open next bar

- Margin Factor : 1

3) Strategy

- Buy at market : ConsecDown(Close1) is equal to 3

- Sell after 5 bars

Backtest Result :

1) Wealth-lab 8 Build 14 PC version

- APR : 1.94 %, QQQ APR : 15.92%

2) Web Builder

- APR: 11.97%, QQQ APR : 15.93%

1) Backtest Data

- Backtest data : DOW30

- Data scale : Daily

- Data range : 2012-09-10 ~ 2022-09-07

- Benchmark : QQQ

2) Position Sizing

- Starting Capital : 100000

- Size : Percent of Equity

- Percent : 20

- Basis Price : Market Open next bar

- Margin Factor : 1

3) Strategy

- Buy at market : ConsecDown(Close1) is equal to 3

- Sell after 5 bars

Backtest Result :

1) Wealth-lab 8 Build 14 PC version

- APR : 1.94 %, QQQ APR : 15.92%

2) Web Builder

- APR: 11.97%, QQQ APR : 15.93%

Rename

It's striking that your report is missing the crucial thing: data provider (or even a question "which data does the WebBuilder use?"). Like whatever data the two different products run the strategy on, doesn't mean a thing. But it does. Assuming the WB runs on QData, to ensure a meaningful comparison you should check QD in the Data Manager (Historical tab) and put it right on top.

The "Dow 30" DataSet in Wealth-Lab 7/8 uses Wealth-Data, which includes the Dow 30's historical components. The Website tests using only the current Dow 30 symbols with our "Q-Data" source.

There have been a handful of changes in the Dow 30 in the last 10 years, but most recently in August 2020, CRM, AMGN, and HON replaced XOM, PFE, and RTX.

Probably if you limit the test to the last 2 years, AND, use Transaction Weight in your entry condition, the results should be very close.

There have been a handful of changes in the Dow 30 in the last 10 years, but most recently in August 2020, CRM, AMGN, and HON replaced XOM, PFE, and RTX.

Probably if you limit the test to the last 2 years, AND, use Transaction Weight in your entry condition, the results should be very close.

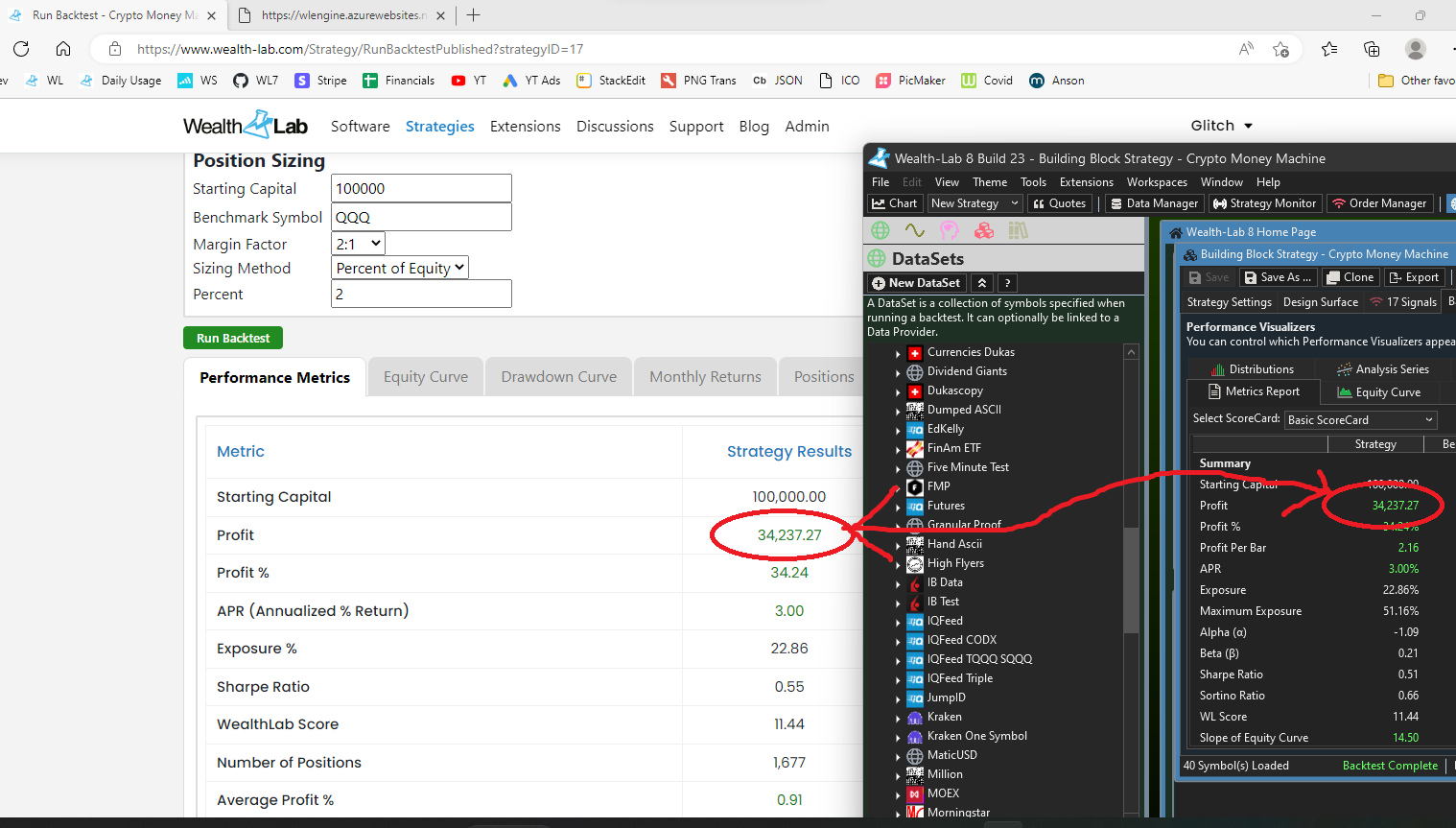

I ran into this same problem too with WL and WB. I back tested a strategy with identical entry/exit signals. And I went back and used both Q-Data and Wealth Data for 10 years back test for a daily strategy. And I also am getting widely different results. Any reason this is happening?? The backtest is only being done on one symbol- TQQQ

First of all, are the results consistent if you run the strategy in WL8 more than once?

yes, they are consistent across WL8.

Interesting, here are my results. When I ensure that ALL settings are identical, and there are NO NSF positions in the backtest, my results match to the penny.

Cone: Even for the Dow 30 current, the web backtester uses WealthData, not QData. QData is only used if there is a symbol not supported by WealthData.

Cone: Even for the Dow 30 current, the web backtester uses WealthData, not QData. QData is only used if there is a symbol not supported by WealthData.

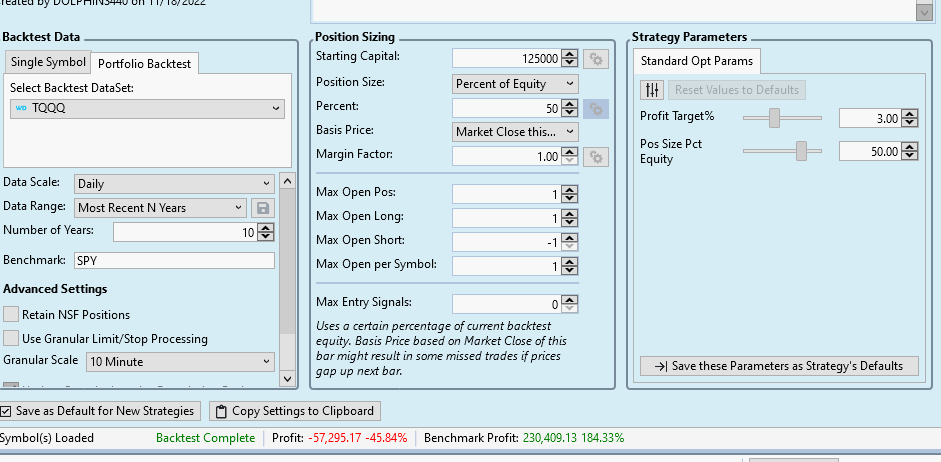

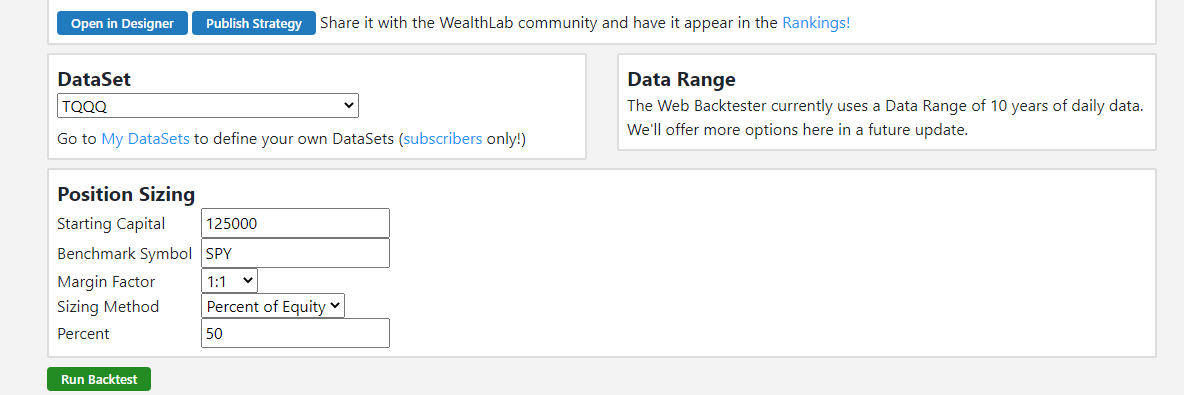

No matter what I do, am I'm using Wealth Data for the daily backtest on TQQQ, the results do not match. One shows a profit of over $200,000, the other shows a loss of over -$50,000. HUGE differences. I have triple checked the entry/exit triggers and they are identical.

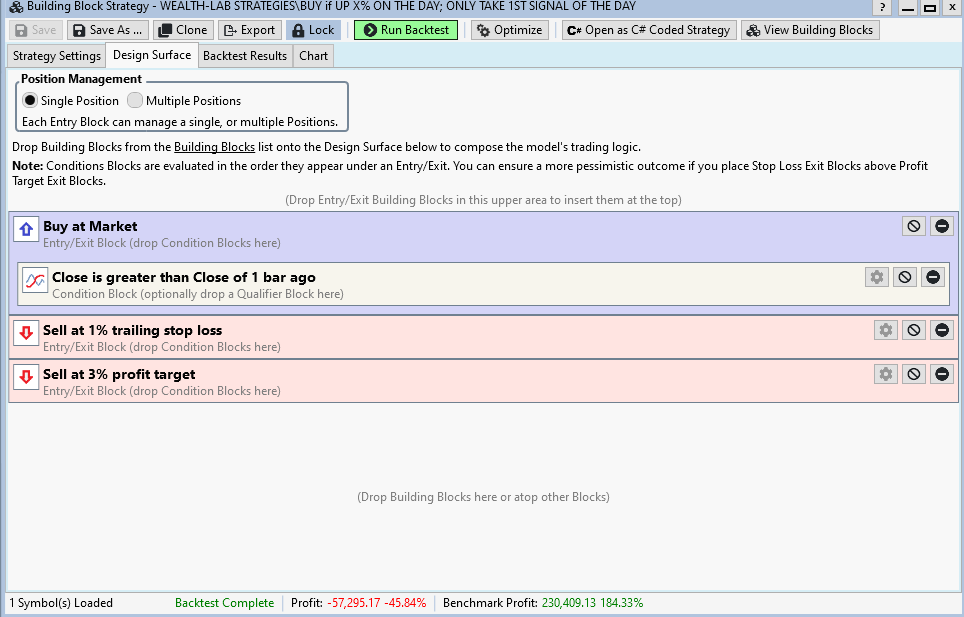

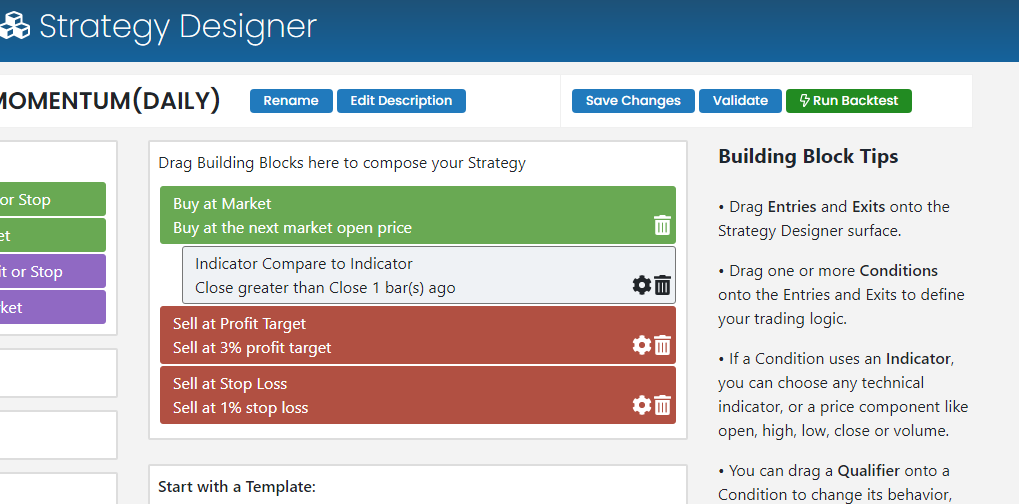

There's actually a subtle difference in the strategy that makes a huge difference in the results - the order of the exits. On your web strategy, the profit target is first, and on your desktop it's last.

For this particular strategy and the TQQQ test data, the order of the exits are especially important. The volatility of TQQQ makes it likely for both exits to be hit on nearly every bar. Without knowing the order of the trading "intra-daily-bar" the exits are processed in order, top to bottom. If the profit target is first, the result will be optimistic. Likewise, if the stop loss is first, the result will be pessimistic (but probably closer to the truth for this strategy).

Note that even though it's a valid case for this strategy, blocks cannot currently program an exit on the entry bar. Consequently, this strategy will always hold the position overnight.

Lesson learned:

When designing a strategy, you should be pessimistic always. The order of exists should be:

1. market order conditions first,

2. and then stop losses,

3. and finally profit targets

Aside:

Although I shouldn't have been, I was a little surprised that the Advanced setting for granular processing (WealthLab desktop) doesn't have an effect. That's because this option is used only for prioritizing trade entries in cases of limited buying power for multiple symbols.

For this particular strategy and the TQQQ test data, the order of the exits are especially important. The volatility of TQQQ makes it likely for both exits to be hit on nearly every bar. Without knowing the order of the trading "intra-daily-bar" the exits are processed in order, top to bottom. If the profit target is first, the result will be optimistic. Likewise, if the stop loss is first, the result will be pessimistic (but probably closer to the truth for this strategy).

Note that even though it's a valid case for this strategy, blocks cannot currently program an exit on the entry bar. Consequently, this strategy will always hold the position overnight.

Lesson learned:

When designing a strategy, you should be pessimistic always. The order of exists should be:

1. market order conditions first,

2. and then stop losses,

3. and finally profit targets

Aside:

Although I shouldn't have been, I was a little surprised that the Advanced setting for granular processing (WealthLab desktop) doesn't have an effect. That's because this option is used only for prioritizing trade entries in cases of limited buying power for multiple symbols.

Thanks Cone! When I reversed(as you advised) the TSL% and the take-profit% so that WB = WL8, the results were almost identical. They were still off a bit, but close enough that I'm satisfied with the results. But I had a follow-up question to what you said-- "Note that even though it's a valid case for this strategy, blocks cannot currently program an exit on the entry bar. Consequently, this strategy will always hold the position overnight."

Your Response

Post

Edit Post

Login is required