A little refinement of the strategy I was able to get a very good return on the DOW30. I used the "Percent Volatility" Pos Sizer to increase the profits, and I noticed the following thing, each time I run the strategy, symbol selection/profits changes. This would be understandable if there were NSF positions, but they are zero. Why does this happen? Also wanted to ask if anyone has already tested this strategy, there are any things to pay attention at, so it doesn't turn out to be a tester-only profitable?

Rename

Please see FAQ: Every time I run a Strategy I get a different result. Why?

Eugene, it's not NSF related, even Maximum exposure is ~80%.

It can happen because you issue a stop and a limit on the same bar, and there are cases where both COULD be hit on the same bar.

Glitch, isn't granular processing made to avoid this? I have tested on 5min and profits differ

Are you sure you have enough intraday data to cover the entire backtest period for all symbols?

I have tested both on wealth-lab data for the last 100 days + granular and the opposite on saved 1h quotes scaled to daily, unstable profits on both options

QUOTE:It does not. Granular processing is currently used only to assign a Transaction.Weight based on the intraday time of day for entries. Nothing is done for exits, and, in this case, I think the outcome is randomized by design (Glitch would have to confirm that).

Glitch, isn't granular processing made to avoid this? I have tested on 5min and profits differ

Granular processing would need an feature request upgrade to fix that.

Right, I double checked too and granular processing currently works for ENTRIES only, the unstable profits in this case are to be expected.

There's something we're going to have to resolve in the backtester. This strategy is getting a peeking result without peeking because it favors the limit exit over the stop.

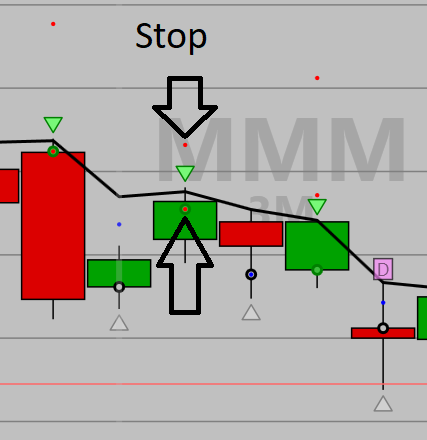

The way the strategy's stop order is calculated, it will almost always execute at the open the next day. Here's just one example that shows how the limit order was rewarded instead of executing the stop right at the the open.

The way the strategy's stop order is calculated, it will almost always execute at the open the next day. Here's just one example that shows how the limit order was rewarded instead of executing the stop right at the the open.

Good catch, resolved this for the next build!

Your Response

Post

Edit Post

Login is required