I've created or evolved over 2000 strategies these past few years and this one, after comparing them all against one another (on Data Scale, Range, Pos'n Size, et al) always seems to survive among the top 20 winners, given my appetite for risk/reward. So thanks for this, #nkrastins !

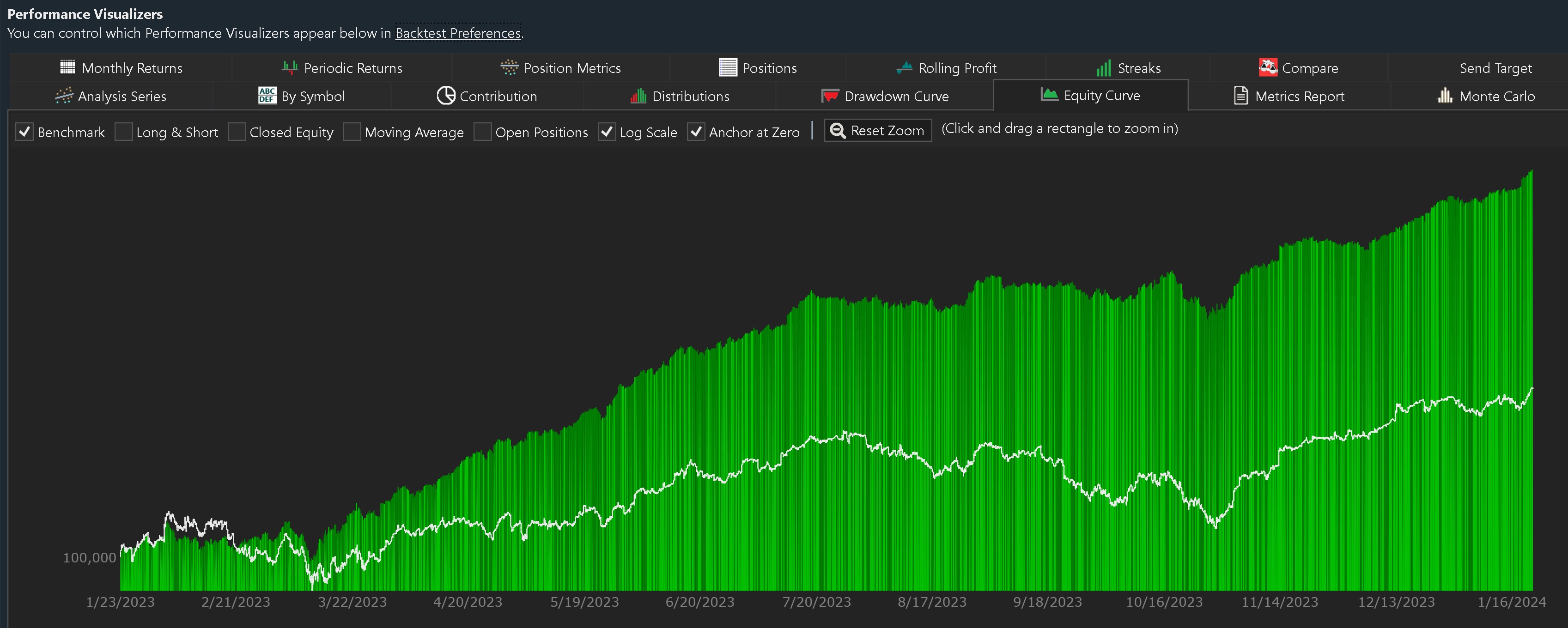

The problem, for me, is with the very high Draw Down.

I've spent countless hours optimizing this strategy for a lower DD, while maintaining the lowest time in the trade, even at the cost of a lower APR, so long as the Win% remains in the 66%-70% level.

Can you offer an suggestions ... which might allow it's users to continue "dancing in the door jamb"?

The problem, for me, is with the very high Draw Down.

I've spent countless hours optimizing this strategy for a lower DD, while maintaining the lowest time in the trade, even at the cost of a lower APR, so long as the Win% remains in the 66%-70% level.

Can you offer an suggestions ... which might allow it's users to continue "dancing in the door jamb"?

Rename

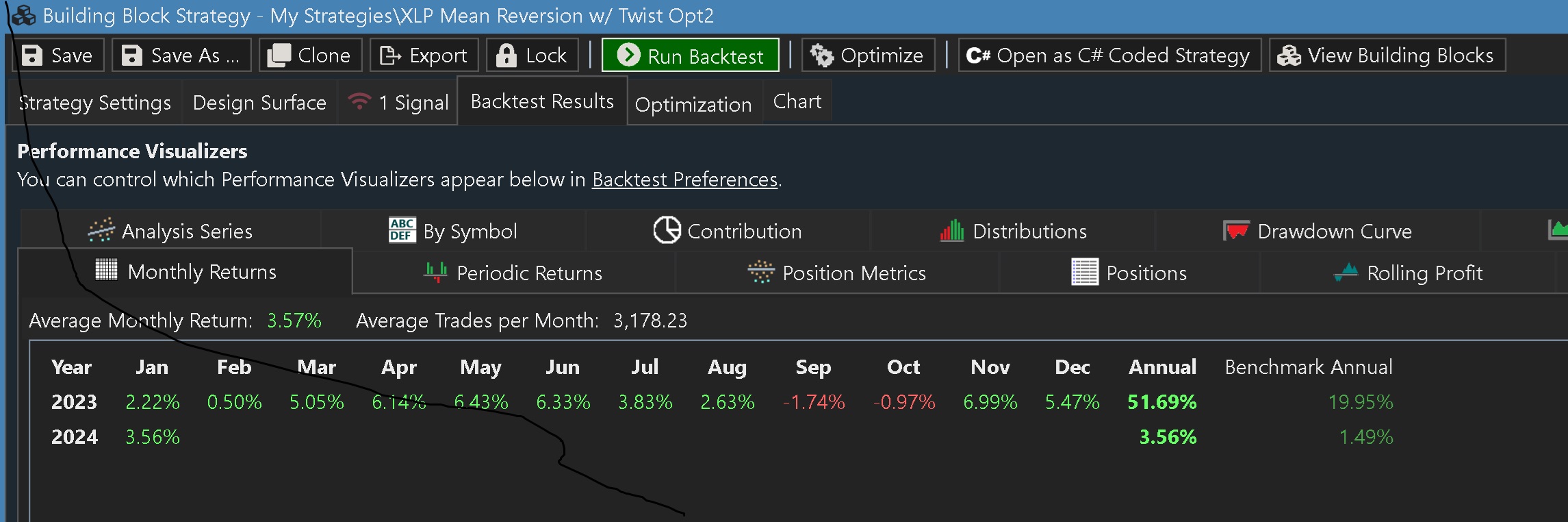

Can you post your monthly returns backtest tab screenshot? I wasn't able to get some decent results. Which dataset are you running this strategy on?

Sure thing, forthcoming.

For this very simple example, I'm using a dataset of QQQ and SPY to be able to give you a full year of data. And I'm using GLD as a qualifier symbol for the second condition block. I commit $100K to the strategy and my Pos'n size is 50% and I'm trading on the minute. I don't trade on the day, so I can't say how this would produce on that scale.

From a practical and risk-based standpoint, I like this strat because I'm in for an average of about 5 minutes, and I'm right most of the time, and still, it beats the spy's APR. But, as I mention in my post above, the DD is too high, so I reached out for advice from the WL community on that.

And, the numbers get even better when you use the WL100 data set for example, and then drop the Pos'n size to say, 1%. But in either case, you can see how important it is for me to be able to Auto Trade through my broker (TD Ameritrade) which has been a problem for some of us lately.

So, premature kudos again to @nkrastins, pending community review of this strats results, at least on the 1 min.

For this very simple example, I'm using a dataset of QQQ and SPY to be able to give you a full year of data. And I'm using GLD as a qualifier symbol for the second condition block. I commit $100K to the strategy and my Pos'n size is 50% and I'm trading on the minute. I don't trade on the day, so I can't say how this would produce on that scale.

From a practical and risk-based standpoint, I like this strat because I'm in for an average of about 5 minutes, and I'm right most of the time, and still, it beats the spy's APR. But, as I mention in my post above, the DD is too high, so I reached out for advice from the WL community on that.

And, the numbers get even better when you use the WL100 data set for example, and then drop the Pos'n size to say, 1%. But in either case, you can see how important it is for me to be able to Auto Trade through my broker (TD Ameritrade) which has been a problem for some of us lately.

So, premature kudos again to @nkrastins, pending community review of this strats results, at least on the 1 min.

Your Response

Post

Edit Post

Login is required